Black Book: Market Insights Report

Black Book recently published an update to their Weekly Market Update.

Black Book recently published an update to their Weekly Market Update.

BLACK BOOK – Black Book recently published an update to their Weekly Market Update.

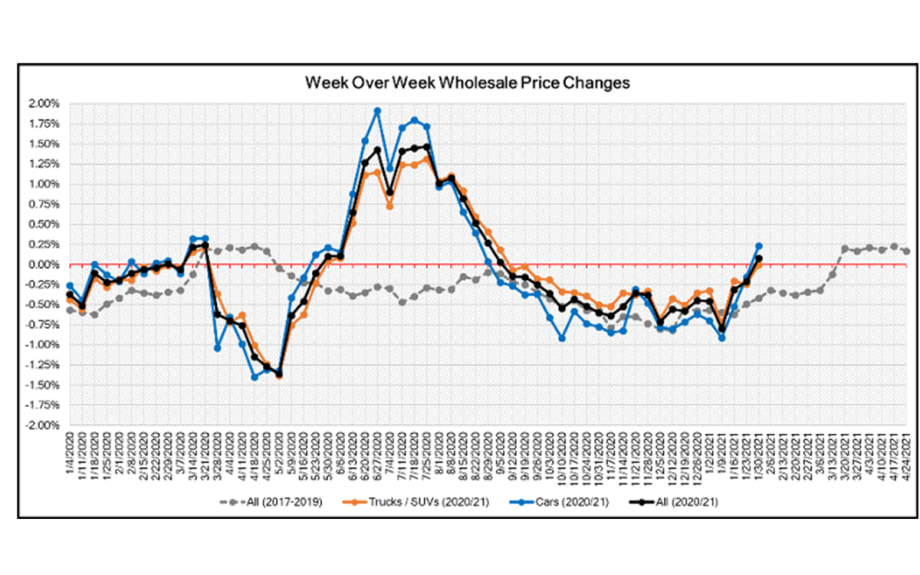

Wholesale Prices, Week Ending January 30th

Wholesale prices reversed their twenty-week trend of declines and finished last week with the overall market increasing in value. The largest gains were in the Car segments, but many of the Truck segments also had week-over-week gains.

This Week Last Week Historical Average

Car segments 0.23% -0.16% -0.42%

Truck & SUV segments 0.00% -0.24% -0.37%

Market 0.08% -0.21% -0.42%

Car Segments

Sporty Cars, both mainstream and Premium, saw signs of Spring this past week with increasing values. Premium Sporty Cars have had only minimal decreases over the past fourteen weeks, but Sporty Cars had twenty-two weeks of declines for a -0.51% average rate of weekly change. Traditionally, the Sporty Car segment begins to show strengthening in February.

This was the second week of increases for the Compact Car segment with the rate of increase growing this week to 0.23%, compared to 0.06% the week prior.

Truck Segments

Full-Size Crossovers experienced a fourth week of gains, last week being the largest of the gains at 0.10%.

Full-Size Pickups ended 2020 up 8.7% and have now begun to climb again. Two weeks ago, the segment experienced stability with a 0.00% weekly change, but the rate of increase rose to 0.09% last week.

The Small Pickup segment also showed signs of strengthening this past week with an increase of 0.13%. This is after twenty-one weeks of declines, for an average weekly change rate of -0.52%.

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. The question still remains whether we will go back to normal seasonality in 2021.

Retail (Used and New) Insights

New inventory levels remain low, especially in the Full-Size Truck and SUV segments, which are continuing to push dealers to look for good used substitutes to offer consumers. On the used side, dealers are preparing their inventory for the potential of a spring market as well as the potential of another round of direct stimulus payments to consumers, which may increase the demand for used vehicles.

The global microchip shortage news continues to be another hot topic in the industry, but this past week there was some positive news with the announced commitment by the Taiwan Semiconductor Manufacturing Company to prioritize chips for automakers. HIS Markit is estimating that the chip shortage could have lingering effects into Q2 and possibly Q3.

Electrification is on the minds of those at the government level and at most of the OEMs.

Biden announced his plans to have the entire government fleet electrified.

Cadillac is beginning the preparation work with their dealer network for the release of the all-electric Lyriq mid-size crossover, set to be released next year. This is the first vehicle in what will be an all-electric line-up for Cadillac by 2030.

Tesla released images of their redesigned Tesla Model S that hasn’t seen any significant changes since the launch in 2012.

GM announced their commitment to stop selling gasoline vehicles by 2035 as part of their goal of becoming carbon-neutral by 2040.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down leading up to the December holidays, and thus resulted in declining retail asking prices over the last several weeks of 2020.

Volume

Used Retail

Used retail listing volume stayed essentially flat since the beginning of the year but remains at levels above where the industry was in January, during the pre-COVID time of 2019.

Days-to-turn have been increasing since November and is approaching historic average level.

Wholesale

Sales rates have been on a continual climb in recent weeks, but last week there was a small decline as sellers held firm to floors. The decline in sales rates was not due to a lack of interest by buyers. The bidding activity on the lanes was very active last week with some deals being passed over as little as $300.

Wholesale volume has shown improvement to start the year, but this past week overall available inventory offered for sale showed signs of once again declining. However, levels are still above the shortages seen last summer. Remarketers are estimating that their available inventory in the pipeline for Q1 is lower than normal.

With remarketers knowledge of limited supply in the pipeline and increased retail demand, they are raising their floors and planning to hold firm.

Originally posted on F&I and Showroom

More Training

ASE Developing ADAS Calibration Credential

The National Institute of Automotive Excellence said its intent with the new technician program is to prioritize practical application and operational understanding over deep electrical diagnostics.

Read More →

Apply by March 31 for Automotive Scholarships

UAF is accepting applications for more than $900,000 in automotive and heavy-duty scholarships for the 2026-27 school year.

Read More →

Combatting the Technician Shortage

RockED and TruVideo have launched a free video inspection certification for automotive schools.

Read More →

The F&I Agent's Roadmap: Mastering the Cold In-Store Visit

Register for Allstate's FREE webinar on Oct. 21

Read More →

APCO Holdings Acquires DealerPRO Training

The addition expands company's footprint in fixed ops training

Read More →

Auto Dealership Training Program Expands

Protective Asset Protection offering is AI-driven.

Read More →

ASE Offers Free Vehicle-Fluids Webinar

Class will share updates on lubricant and filtration technologies in newer models.

Read More →

New ADAS Certification Announced

ASE training is intended to help service departments, shops optimize repair opportunities, customer confidence.

Read More →

ASE Offers Free Testing Webinar in Spanish

The class will give an overview of ASE testing in Spanish, including current tests, test development and test-preparation tools.

Read More →

F&I Conviction

It is not important that the client understands us – it is critical that they know we understand them!

Read More →