Preloads, Profits, and Payment Packing

The F&I industry continues to be plagued by malfeasance at the retail level. Attorney and compliance expert gets P&A executives up to speed.

The F&I industry continues to be plagued by malfeasance at the retail level. Attorney and compliance expert gets P&A executives up to speed.

In an age of tightening front-end gross, dealers search for ways to reserve profits on the vehicles they sell. One such tactic is the practice of including the price of products or services on every vehicle sold before a customer walks on the lot. The products or services are thus called “preloads.”

Overstating the value of collateral, once the RISC is purchased by a finance source, can be construed as bank fraud.

Is preloading legal or illegal? The answer, of course, is “Yes” — it just depends on how you do it.

Before we parse this topic, let’s remind ourselves of the “Guiding Principles of Compliant F&I”:

Be truthful.

Be transparent.

Be reasonable.

Document every step of the process.

Befriend a lawyer.

What follows is how we follow those guiding principles when it comes to preloads.

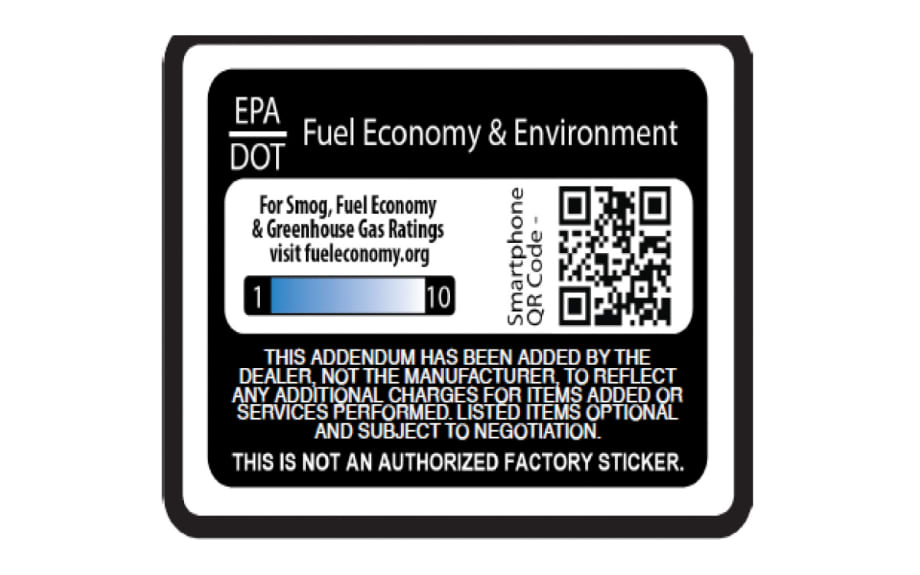

Not What Monroney Had in Mind

Because preloads need to be disclosed somewhere, let’s begin with the addendum sticker. In the beginning (1958, anyway) was the Monroney label, that mandatory factory-installed sticker on every new car that sets forth MSRP, standard equipment and options, and average fuel economy.

Sometime later, the first dealer thought of adding an addendum sticker that looked just like the Monroney label. The idea, one assumes, was to create the illusion that the addendum sticker was factory mandated, and the products listed thereon were somehow as mandatory as the engine displacement identified on the Monroney label.

See Guiding Principles 1, 2, and 3, above.

To be clear, in order to be transparent, any preloads need to be disclosed right up front and in a manner that is not confusing or misleading. An addendum sticker is a fine way of doing that. Just be sure the sticker doesn’t look like a continuation of the Monroney label. Different colors, fonts, and the dealership logo are ways to accomplish this. Better still, use all three.

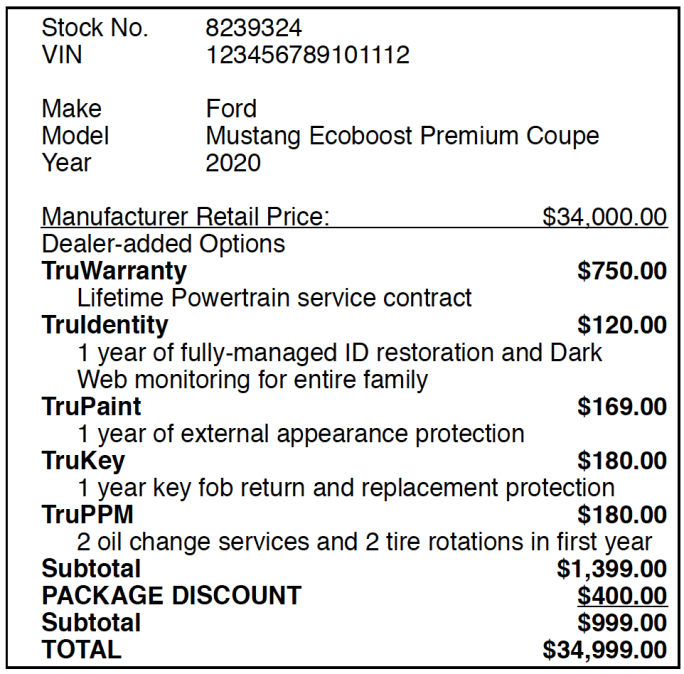

Preloaded products should be individually listed and priced. Price them as if they were being sold individually in the F&I box, then, include a discount for purchasing the bundle (if allowed in your jurisdiction). You need to build value. This is one way to do so.

Here’s an example:

Add a final disclosure that states the obvious: “Items listed are optional and subject to negotiation.” Do not hornswoggle customers by implying the preloads are mandatory. This is a car deal — everything’s negotiable! Don’t try to hide behind a sneaky tactic; build value instead. And never, ever, try to lever the preload into sales pressure. (“Sure, you can get the truck without the bedliner, but it will take 16 weeks for delivery.”)

Preloaded products may be either “hard adds” or “soft adds.” What’s the difference? Hard adds are items actually attached to the vehicle, such as a spray-on bedliner on a pickup truck or a Bose eight-speaker stereo system. Hard adds increase the value of the vehicle itself. Soft adds do not. The distinction is crucial.

Because soft adds, such as service contracts, etch, and key replacement, do not enhance the value of the vehicle itself, their cost should not be included in Line 1 of the retail installment sale contract.

Why? Because Line 1 sets forth the cash price of the vehicle, plus accessories (meaning hard adds), taxes and mandatory fees. In other words, the value of the collateral.

Bank Fraud and Payment Packing

Overstating the value of collateral, once the RISC is purchased by a finance source, can be construed as bank fraud.

Don’t do bank fraud.

Soft adds belong in Line 4, “Other Charges Including Amounts Paid to Others on Your Behalf,” unless you’re in California. In California amounts paid to others goes in Line 5.

What about “squishy adds,” like paint and fabric protection? Something — a chemical treatment — has actually been added to the vehicle. Because the bulk of the value is the guarantee backing up the chemicals’ performance, I would treat them as soft adds.

But in case of doubt, contact your bank rep and ask. Document the response (Guiding Principle 4). And once documented, run it past your lawyer — who wants to trust legal advice from a bank rep? See Guiding Principle 5.

Why the care to properly disclose preloads? Because if you don’t, your preload program could be construed as payment packing.

Don’t pack payments.

The most succinct official definition of payment packing goes back to a 1999 resolution of the National Association of Attorneys General: “‘Packing’ is the deceptive practice of misrepresenting monthly payments to consumers during auto sales and lease negotiations in order to facilitate the sale of automobile related products and services.”

Implicit in NAAG’s definition of packing payments is the necessity of an accurate monthly payment. And that payment must be based on the actual cost of the vehicle, plus taxes and mandatory fees. If the vehicle includes preloaded products, those products must be unambiguously understood and agreed to by the customer.

Accurate and Defensible

If there is one fixed star in the F&I heavens, it is this: Customers must be presented with a payment that is accurate and based upon a representative term and APR.

What term? Your dealership’s actual current average term is best. The national average is also defensible (69 months as of this writing). Reasonable and common terms can work (say, 60 and 72 months). But using a 36- or 48-month term when no one in your market finances at those terms is not defensible, and creates a deceptively high monthly payment quote.

What APR should you use for first pencil quotes? Either the 90-day rolling average for your store (which can become unwieldy and fall into disuse) or, more simply, your captive finance source’s Tier 2 rate. Of course, once a customer’s credit is pulled (with the customer’s express permission, duh), the actual APR for which the customer qualifies should be used.

Assuming the APR and term are accurate and representative, what is the amount to which they are applied? In a transaction with no preloads, that’s easy: the vehicle alone (with taxes and fees). But in a transaction with preloaded items, the base payment would include the price of those items. The inclusion of those items and their price must be clear and unambiguous.

It is a best practice to get the customer’s signature near that disclosure to confirm understanding and consent. In the absence of a clear disclosure and evidence of understanding and consent, you have — at least — the appearance of payment packing.

How can you demonstrate that a transaction was on the up-and-up? One way, is to list two payments on the first pencil: “base vehicle only” and “vehicle as offered,” (which would include the preloaded products). Don’t fear the payment differential; embrace it and build value.

But two payments at the same APR and term could itself seem confusing, and confusion is the very thing we’re trying to avoid. One large dealer group permits a customer signature on the addendum sticker, buyer’s order, or worksheet to demonstrate understanding and consent. The point is to unambiguously confirm that the customer knew exactly what the customer was getting.

Once the process gets to the F&I menu presentation, be sure to (accurately) list the vehicle price with the preloads (if accepted by that point) as the starting point. On any accept/decline acknowledgement sheet the customer signs at the end of the menu presentation, be sure the accepted/declined options are identified as additional options. This will highlight the fact that the preloads were included in the transaction before the menu presentation began.

Applying the Guiding Principles of Compliant F&I

Here are the specific steps to take to reduce the risk of packing payments when preloading products:

Disclose that the preloaded products are dealer-added options and subject to negotiation.

DO NOT include soft adds in Line 1 of the RISC until you’ve checked with your bank rep and local attorney.

Clearly disclose the inclusion of the preloaded products in the first pencil — and get the customer’s signature to document understanding and consent early in the process.

Don’t gouge. Be sure the preloaded products are priced appropriately, perhaps at a meaningful discount below what they would cost individually if purchased separately.

If the product is a hard add and it’s on the addendum sticker, be sure it’s actually on the vehicle!

Review the Guiding Principles of Compliant F&I.

Memorize Guiding Principle 5.

James Ganther is president of Mosaic Compliance Services and co-founder of Automotive Compliance Education, a training and industry certification company.

Originally posted on P&A Magazine

More Compliance

RockED Offers Free FTC Pricing Education Series for Dealerships

The program is designed to help dealers, managers and front-line teams get more information about Federal Trade Commission pricing enforcement, advertising transparency and evolving regulation.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

AAMS Training and Mosaic Compliance Services Merge

The strategic combination is intended to expand technology-driven compliance solutions for the automotive industry.

Read More →

The Jurisprudence of Pricing

Legal concept helps makes sense of California’s recently passed version of the failed federal CARS legislation.

Read More →

Trump 2.0 and Enforcement Priorities

The upshot is don’t relax, because regulation indeed continues.

Read More →

June Is Automotive Service Professionals Month

Observance is opportunity to thank technicians for their crucial role in auto retail.

Read More →

Cox Automotive Releases Compliance Guide

New edition walks auto dealers through relevant regulations for 2025.

Read More →

Trump 2.0 and Retail Automotive

Administration’s plans should generally bode well for the industry.

Read More →

CARS Rule Update: 5th Circuit Oral Arguments Recap

In this video, Jim Ganther of Mosaic Compliance Services, recaps the key takeaways from the oral arguments in the critical CARS Rule case, including potential outcomes and what dealers should do to stay ahead of compliance changes.

Read More →

State of the CARS Rule, Part 3

The players in the automotive industry should coordinate their responses to this pending regulation.

Read More →