2011 Auto Finance Survey Results

This year marks the eighth annual Auto Finance Survey administered by Auto Dealer Monthly, and many positives were found in the results.

F&I Office

This year’s Auto Finance Survey revealed that auto financing has continued to improve throughout 2011. This year marks the eighth annual Auto Finance Survey administered by Auto Dealer Monthly, and many positives were found in the results.

For example, respondents (the majority of whom are dealer principals and finance managers) reported improvements in the areas of product penetration in the finance office, deal approvals, availability of financing and subprime sales volume. Below is a detailed look at this year’s survey findings:

F&I Office

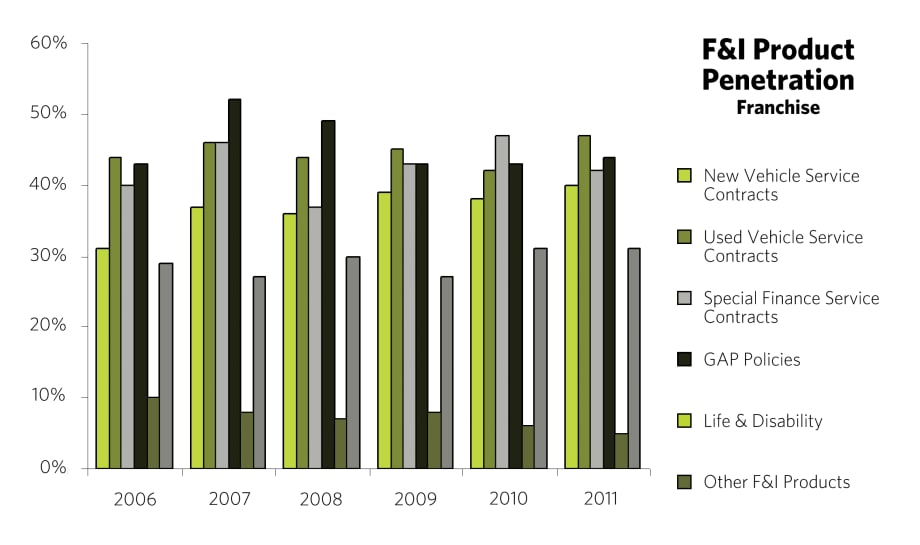

In the F&I office, franchise dealers saw a small increase in penetration of new-vehicle service contracts. They reported 40-percent penetration this year, which also happens to be the highest penetration ever reported in the history of the finance survey. Used-vehicle service contract penetration was the highest penetration reported this year among F&I products for franchise dealers, with 47-percent penetration (a 5-percent increase over last year). Service contract penetration on special finance deals declined this year to 42 percent, compared to last year’s 47 percent.

GAP penetration remained steady for franchise dealers, who reported a rate of 44 percent so far in 2011. Life and disability insurance is continuing to decline. The “other products,” which includes a wide range of products from etch to vehicle appearance products remained similar to last year as well.

The average F&I income per deal reported by franchise dealers this year was $1,028, and almost every franchise dealer respondent reported an increase in F&I income per deal this year compared to last year.

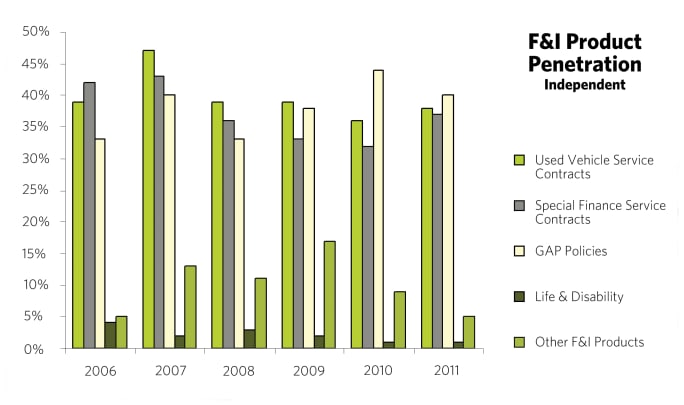

For independent dealers, service contract penetration saw a modest improvement as well. Their used-vehicle service contract penetration this year was 38 percent. Additionally, they saw a 5-percent increase in service contract penetration on special finance deals, reporting 37-percent penetration this year. GAP penetration for independent dealers is running at 40-percent penetration this year, slightly less than their franchise counterparts. So few independents sell life and disability insura

For independent dealers, service contract penetration saw a modest improvement as well. Their used-vehicle service contract penetration this year was 38 percent. Additionally, they saw a 5-percent increase in service contract penetration on special finance deals, reporting 37-percent penetration this year.

GAP penetration for independent dealers is running at 40-percent penetration this year, slightly less than their franchise counterparts. So few independents sell life and disability insurance products that they barely have a 1-percent penetration rate for these products. Independent dealers tend to fair significantly worse than their franchise brethren, do much in part that many of the products sold in the category tend to revolve around new vehicles. As such, they reported only a 5-percent penetration so far in 2011.

When it comes to average F&I income per deal, independent dealers are considerably lower than franchise dealers, with a reported average F&I income per deal of $421.

Franchise Dealers’ Top Finance Companies

For the second straight year, dealers tabbed Ally Financial their number one choice for their prime credit score customers (700+ credit score). The former GMAC, now working with a wide array of both franchise and independent dealers, easily outdistanced Bank of America for the honors. The majority of franchise dealers said their top prime finance company gets between 40 and 50 percent of their deals with scores over 700. They reported sending high percentages of their prime business to their number-one choices in this segment due to the finance companies’ rates, advances, ease of funding and lease programs.

In the 660 to 699 credit score segment (also referred to as the near-prime segment), Ally was again the leading choice for franchise dealers. They’re not sending quite as much business to their top choice in this segment compared to the 700-plus segment, but they’re still quite reliant on their top choice for 660 to 699 scores. Most of the franchise dealers reported sending 30 to 40 percent of their business in this segment to their top finance company. They stated the main reasons they send their business to a finance company in this segment relate to rates, advances, funding, floor planning and relationships.

The 610 to 659 credit score segment – the Tier One subprime credit tier – was led, yet again, by the popular Ally, but narrowly over Wells Fargo. Interestingly, there was a strong emergence this year by Capital One Auto Finance, as well as the fourth most popular, Bank of America. In this tier, franchise dealers are still sending quite a large percent of their business to their number-one picks, stating their top choices get 40 percent of their deals with scores of 610 to 659. The main reasons these finance companies get so much of their dealers’ business in this tier is mainly due to the depth of the companies’ buying and the relationships they keep. Other important reasons dealers rely on these companies include advance and rate.

With Tier Two going deeper into the subprime spectrum, the 540 to 609 credit score range revealed a different top finance company for franchise dealers. Here, largely due to their national footprints, Capital One Auto Finance was the favored source, followed by GM Financial/AmeriCredit, Wells Fargo and Ally Financial. It should be noted that many smaller companies such as Regional Acceptance, Exeter Finance and even Condor Financial received very favorable responses from dealers in their market areas. Dealers reported that 30 to 40 percent of their deals in this tier go to their number-one source. In this segment, dealers said the two main factors playing into their decisions about where to place deals are relationship, advance and rate.

The top finance source named by franchise dealers for Tier Three, the 485 to 539 credit score range, was GM Financial/AmeriCredit, followed very closely by Capital One Auto Finance. It was apparent that the swing was by the General Motors franchise dealers reporting excellent success with subvented loans on select new vehicles for tougher credit customers. Loyalty wasn’t quite as strong in this segment; getting deals done was listed as more important. Most dealers reported their top source in

The top finance source named by franchise dealers for Tier Three, the 485 to 539 credit score range, was GM Financial/AmeriCredit, followed very closely by Capital One Auto Finance. It was apparent that the swing was by the General Motors franchise dealers reporting excellent success with subvented loans on select new vehicles for tougher credit customers. Loyalty wasn’t quite as strong in this segment; getting deals done was listed as more important. Most dealers reported their top source in this tier gets between 20 and 30 percent of their deals. Relationships and fees play a big factor in with whom dealers work.

In the tough-to-get-approved Tier Four segment of 300 to 484 scores, franchise dealers reported Santander was their top choice. Similarly, for deals with no credit score, Santander was also the most popular, followed closely by Credit Acceptance and Westlake Financial. In this segment, it’s all about the ability to get approvals and what makes the most sense for the dealership. Many of the companies working within these areas have very different programs. Some are point of purchase, such as Santander, and others such as Credit Acceptance are portfolio based. So that plays a factor in dealers’ decisions as well.

Independent Dealers’ Top Finance Companies

A continuing challenge for independent dealers is creating relationships with finance companies because many companies choose to do business with only franchise dealers. While some of these franchise-exclusive finance companies will do business with independents, they’re extremely picky regarding which independents they’ll do business with. Hence, independent dealers reported credit unions as their top finance sources in the top three credit-score tiers (700-plus, 660 to 699 and 610 to 659). They reported sending high percentages of their prime, near-prime and subprime business to credit unions due to the rates and terms at which they’ll finance vehicles for customers.

When independents work with customers with scores in the 540 to 609 range, their top choice shifted. The top finance company they named in this segment was Westlake Financial, which happened to be the top company named in the 485 to 539 credit score tier as well. In these two segments, every independent dealer reported that more than 50 percent of their deals went to their number-one source.

When independents work deals with credit scores below 610, securing financing on deals that are profitable for the dealership can be difficult. To fund deals in the Tier Two subprime arena, they’re reliant on Chase Custom, GM Financial/AmeriCredit and Regional Acceptance. As credit moves into the Tier Three and Tier Four areas, independents turn to Credit Acceptance and Westlake Financial most often. Certainly for many independent dealers, local credit unions, banks and smaller local finance companies can play a great importance, based on the strength of individual relationships.

An auto finance niche that continues to perform consistently for both franchise and independents is the bankruptcy niche. Dealers mentioned four finance companies they were reliant on to get these deals done: Consumer Portfolio Services (CPS), Tidewater, Prestige Financial and Friendly Finance. It’s tough to measure these companies side-by-side due to the fact that they cover varying territories. CPS has the widest reach among the four companies named, serving dealers in 45 states. Ti

An auto finance niche that continues to perform consistently for both franchise and independents is the bankruptcy niche. Dealers mentioned four finance companies they were reliant on to get these deals done: Consumer Portfolio Services (CPS), Tidewater, Prestige Financial and Friendly Finance. It’s tough to measure these companies side-by-side due to the fact that they cover varying territories. CPS has the widest reach among the four companies named, serving dealers in 45 states. Tidewater is in 26 states, almost evenly spread out among the West (10 states), South (nine states) and Midwest (eight states) regions. Primarily working in the West region is Prestige Financial. Eleven of the 21 states Prestige serves are in the West, five are in the South, four are in the Midwest and one is in the Northeast region. Friendly Finance is in 12 states (six in the Midwest and six in the South). (Numbers based on U.S. Census Regions)

Subprime Finance

Many of this year’s franchise survey respondents said much of their business is subprime; 21 percent of them said 90 percent or more of their business is subprime. At the opposite end of the spectrum, 53.6 percent of franchise respondents said subprime is less than 20 percent of their business. According to survey results, a higher percentage of independents are reliant on subprime deals. More than half of independent dealers said subprime deals account for more than 70 percent of their business.

Over the last three months, compared to the same period in 2010, 55.5 percent of franchise dealers said their subprime credit volume is better or much better, and 30.1 percent said it’s about the same. Among independents, 75 percent said their subprime credit volume is better or much better. This indicates the subprime market is growing and is wide open for those who know how to capitalize on it.

The lowest credit score both franchise and independent dealers can routinely get approved by prime finance sources was between 600 and 619. The number of franchise survey respondents who reported this was a bit lower than in past years (29.6 percent), indicating prime finance sources are beginning to get more aggressive in their approvals of subprime deals. A small percent of independents reported they can get deals with scores in the 580 to 599 range financed by a prime source. Several franchise dealers even reported the 540 to 559 credit score segment was being served by some prime sources. Getting approvals on deals with scores that low is mainly due to strong relationships between dealerships and finance companies.

Franchise dealers reported being authorized to do business with nine subprime finance companies, which is two more than last year. However, the number of subprime finance companies they regularly do business with hasn’t changed from last year; franchise dealers again reported they’re regularly funding subprime deals with five of the companies with which they’re authorized to do business.

Independents also saw an increase in the number of subprime finance companies they’re authorized to do business with. This year, they reported being signed up with eight companies, up from last year’s five. However, they’re regularly funding deals with only two or three of the eight they’re signed up with.

In summary, both franchise and independent dealers in general report a steadily improving auto finance climate, with more consistency among the finance companies and dealership operations than what they have reported over the past five years. With this, and with the attitude among the finance companies serving the industry being generally bullish, dealers should be able to anticipate more of the same over the next six to 12 months.

Vol. 8, Issue 11

More Dealer Ops

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →

IA American Appoints Two Execs

Senior vice presidents of the company's agent and dealer channels chosen to support general agents and help auto dealers with sales and performance.

Read More →

Cox Automotive Acquires Inspection Firm

Full ownership of Alliance Inspection Management, or AiM, meant to unlock growth for Manheim inspection capabilities

Read More →

Assurant Expands Partnership With Holman

Extended collaboration delivers training, products and performance development to 30 newly acquired Holman dealerships

Read More →

Franchises, Throughput Down in First Half

A handful of states see franchise growth through June, while EV sales per store boost overall business in U.S.

Read More →