Black Book: Specialty Market Report

For the second time in as many months, one of the major RV market segments has declined in value, but this time it was the towables, which fell for the first time in almost a year, while motorhomes reversed course and increased, coming in at their second highest value ever.

For the second time in as many months, one of the major RV market segments has declined in value, but this time it was the towables, which fell for the first time in almost a year, while motorhomes reversed course and increased, coming in at their second highest value ever.

BLACK BOOK – Motorcycles and Powersports Market Update

“Since the COVID-19 pandemic began, life has changed in many ways both good and bad; the same goes for the Powersports market. We have seen many changes, from how we interact with customers and others in person, to the availability or lack thereof, of inventory, both new and used. Through it all, one major question has loomed, when does it end, and how do we get back to “normal?” Over the past few months, it has looked at times like regular seasonal market patterns were returning, only to be upended a few weeks later. That trend continues this month with segments sending mixed signals yet again about where we are headed. After the first year of the pandemic, where values to most everyone’s initial surprise only headed upwards, we now appear to be in a still hot market, but with much more volatility as things are trying to work their way back towards more typical patterns of behavior.” – Scott Yarbrough, Senior Analyst, Motorcycle & Powersports

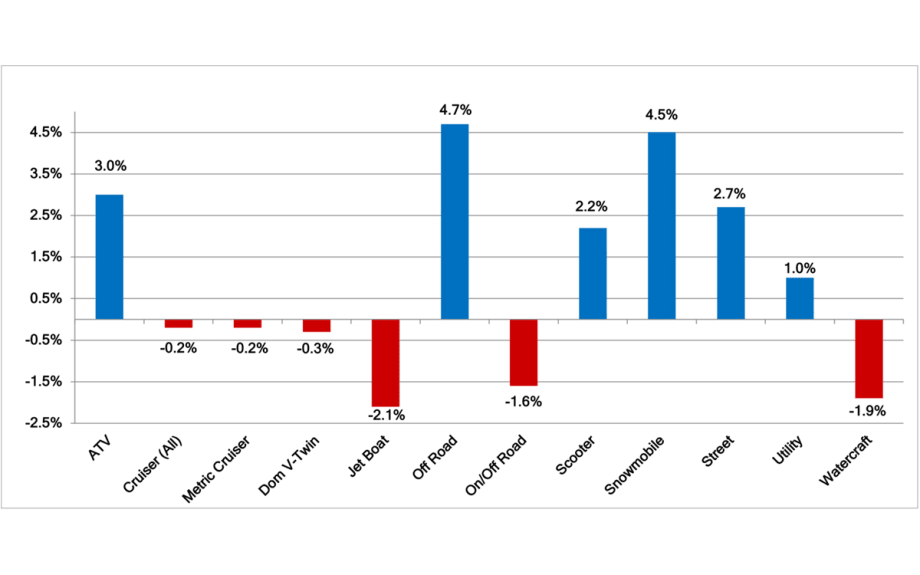

October to November Average Segment Change in Value

COVID-19 Drives Powersports Values up 35.8% vs 2 Years Ago

ATV: 42.1% Snowmobiles: 24.3%

Cruiser – All: 35.9% Street: 26.9%

Jet Boats: 39.8% Utility Vehicles: 47.3%

Off-Road: 35.9% Watercraft: 31.2%

Dual Sport: 27.7% Metric Cruisers: 35.6%

Scooter: 46.4% Domestic V-Twin Cruisers: 28.7%

The chart above is from a presentation we did at the Powersports Finance Summit 2021 last month in Las Vegas. Thank you to those of you who attended, and it was great being able to say hello in person again. The chart shows the total appreciation for each of the major segments we cover from August 2019 to August 2021. The overall appreciation for the entire Powersports industry during that period was 35.8%. As you can see, there is quite a lot of variation between the different segments, with the off-road vehicles, primarily ATVs and Utility Vehicles seeing the largest gains, while Street Bikes and Cruisers have seen smaller, though still extremely large, increases in value.

Snowmobiles, which are the segment with the least value appreciation since COVID started, are quickly gaining on the other segments, with a rise of nearly 4.5% this month (not reflected int the above numbers) and with expected gains as the weather turns colder, are likely to approach or match overall industry rates in the near future.

As noted above, the Powersports market is seeing increasing volatility at the moment as traditional seasonal pricing trends are colliding with current market realities of high demand and continuing inventory constraints on both the new and used side. This was a major topic of discussion at the Powersports Finance Summit 2021, and while there was not widespread agreement on how much prices are likely to go up over the next 6 to 9 months, there was nearly universal agreement that they would indeed increase overall during that time frame. Not until new production catches up with demand, and more normal levels of used units are flowing into the remarketing channels, will “normal” value levels reappear. It is our opinion that this is unlikely to occur until the second half of 2022 at the earliest. Until that time, dealers will need to remain creative in how they both acquire new inventory and in their sales strategies, namely prospecting for vehicles and pre-selling new units while showroom floors remain sparsely stocked.

Recreational Vehicles Market Update

“For the second time in as many months, one of the major RV market segments has declined in value, but this time it was the towables, which fell for the first time in almost a year, while motorhomes reversed course and increased, coming in at their second highest value ever. The direction of the market is best described as “uncertain”, and we’ll be keeping a close eye on it going forward.”– Eric Lawrence, Principal Analyst, Specialty Markets

Wholesale RV Values Mixed Heading Into Late Fall

For Motorhomes (including Class A, B, and C)

Average selling price was $74,990, up $5,037 (7.2%) from the previous month.

One year ago, the average selling price was $57,641.

Auction volume was up 4.9% from the previous month.

The average model year was 2010.

For Towables (including Travel Trailers and Fifth Wheels)

Average selling price was $22,009, down $2,271 (9.3%) from the previous month.

One year ago, the average selling price was $18,638.

Auction volume was down 18.1% from the previous month.

The average model year was 2015.

Industry Highlights

According to the RVIA, the total number of RVs shipped in September reached 55,014, the highest amount ever for any month, and an increase of 32.2% over September 2020. Towables totaled 50,696 units and motorhomes accounted for 4,318. Truck Campers came in at 395, Folding Camping Trailers reached 642, and Park Models were 301. Class B motorhomes (Van Campers) had another outstanding month, with 1,245 shipped. Class As totaled 1,257 and Class Cs finished up with 1,816.

Winnebago Industries announced fourth quarter revenue of $1 billion. This is up 40.4% over the same period in 2020. Gross profit also grew, up to $187.2 million, while their gross profit margin increased to 18.1%. Net income was $84.1 million, an increase of 98% over Q4 of last year.

Megadealer RV Retailer has acquired Aloha RV, adding two locations in New Mexico, bringing their total number of locations to 75.

Kampgrounds of America (KOA), announced that revenues have increased 36.6% year to date, putting them on-track for a record-breaking year.

Baird’s Dealer Sentiment Index showed 71 out of 100 dealers were positive on current conditions, while 61 also were on the 3-5 year timeframe.

Dometic, a major supplier to the RV industry, announced that net sales rose 24% in Q3.

Statistical Surveys, Inc. reported that there were 45,188 retail RV registrations in August, down 25% year over year.

Collectible Cars Market Update

“The beginning of fall is always a busy time as many enthusiasts try to squeeze in one more event before the weather starts to get too cold and their attention turns to winterizing their cars and thinking about what’s going to happen in Scottsdale and Kissimmee in January. The most recent auctions were all very well attended and buyers had no qualms about stepping up and paying serious money for the right cars.”– Eric Lawrence, Principal Analyst, Specialty Markets

Auction Activity

RM Sotheby’s Hershey, Pennsylvania auction was held at the Hershey Lodge during the Antique Automobile Club of America’s Eastern Division Fall Meet. As always, the event featured brass era and classic vehicles and was very well attended, with the auction being one of the highlights of the weekend. Total sales came in at just under $13 million, and the sell through rate was a very healthy 98%. Although it did not break into the top ten sales, a crowd favorite was the immaculately restored 1948 Diamond T 201 Pickup, nicknamed “the Cadillac of trucks”.

Mecum had a very busy October, hosting auctions in Las Vegas, Nevada; Chattanooga, Tennessee; and Chicago, Illinois. These auctions all did quite well, with sales of $22.3 million, $18.7 million, and $21.7 million respectively, with an average sell through rate of 85%. All told, total sales across all three came in at more than $60 million, justifying their nickname of the “October Takeover”. As we have been seeing more and more recently, the top sellers were a mix of traditional muscle cars, mild customs, and restomods.

Bonhams presented the inaugural Audrain Concours auction at the International Tennis Hall of Fame in Newport, Rhode Island. As you would expect from an auction affiliated with a concours and a museum, the vehicles were all beautiful and total sales came in at roughly $9 million with a sell through rate of 79%. On the other side of the Atlantic, in Knokke-Heist, Belgium, the annual Zoute auction saw sales of just over $15 million with a sell through of 85%. The highlight of the sale was a 1994 Bugatti EB110 Super Sport Coupe, one of thirty, which sold for $2.5 million.

Notable Recent Auction Sales Include:

1970 Maserati Ghibli Spyder $572,532 (Bonhams)

1968 Ferrari 365 GTC Coupe $655,500 (Bonhams)

1947 Ford Sportsman Woodie Convertible $104,500 (RM Sotheby’s)

1931 Duesenberg Model J Roadster “Green Hornet” $1,650,000 (RM Sotheby’s)

1962 Ford Thunderbird Sports Roadster $137,500 (Mecum)

1970 Buick GSX Hardtop $121,000 (Mecum)

1968 Shelby GT500KR Convertible $176,000 (Mecum)

1970 Plymouth ‘Cuda 440 6-Bbl Coupe $165,000 (Mecum)

2006 Ford GT Coupe $374,000 (Mecum)

2000 Rolls-Royce Corniche Convertible $151,250 (Mecum)

1970 Maserati Ghibli Spyder Courtesy of Bonhams

Market Trends

The Vintage European/Asian Sports Car segment represents classic “sports cars” in the purest sense of the word. Although most immediate post war European and Asian vehicles were strictly utilitarian, a few lighter hearted enthusiast-type vehicles were part of the mix. As Europe and Asia continued to recover and rebuild in the late 1950s and 1960s, manufacturers expanded their sports car offerings. This genre would include MGs, Alfa-Romeos, Triumphs, Porsches, some Datsuns, Jaguars, BMWs, and many Mercedes-Benz models. These vehicles are really considered to be “timeless”, as their appeal spans multiple generations. The market has its peaks and valleys, but for the most part is very stable. It has recently declined a bit, but has stabilized over the past few months and looks poised to see some increases.

All of the collectible vehicle segments we track increased in value last month, including Muscle Cars, Pony Cars, American Classics, European/Asian Sports Cars, Vintage Exotic Cars, and Classic Trucks/SUVs. As we are coming out of COVID and things have been getting back to normal (hopefully) there has been a lot of pent-up consumer demand, especially for the “fun vehicle” categories, including Boats, Motorcycles/Powersports, RVs, and of course collectible cars and light trucks. With the lack of vehicles at new car dealerships, and the associated price increases of normal used vehicles, we have heard that some consumers are opting for a collectible to use as their daily driver until the supply of regular vehicles increases and prices come back down to more typical levels.

Medium and Heavy-Duty Truck & Commercial Trailer Market Update

Commercial Truck Market Update

“This market is truly amazing! Week after week commercial values continue to raise the soft celling as new production remains well under demand. Over the past couple of weeks, we’ve attended both in-person and online auctions. We are seeing certain highway tractors bring thousands of dollars more than they did a few years ago. This is even more impressive when you consider the increases in mileage and overall wear on the equipment. The chart below shows the average monthly adjustment trends for each segment from classes 4-8. We’ve seen nothing but strength in all sales channels and expect this to continue through next year. Continued supply chain issues have forced many to extend their previous expectations for when production will meet demand. With over 19 months of below normal new model production for classes 4–8 and commercial trailers, we do not expect supply to catch up with demand until after the first quarter of 2024. Used prices will continue to increase through Q2 of next year before reaching a soft ceiling that is expected to last the remainder of the year. We expect to see softening in used pricing beginning as early as the second quarter of 2023 for commercial trucks and trailers. “– Josh Giles, Principal Automotive Analyst, Valuations & Residuals

Heavy-Duty Trucks and Tractors

The chart above shows the monthly adjustment trends for each segment within the Heavy-Duty market.

Heavy-Duty Over-the-Road (OTR) values increased 1.6% from October to November, compared to the 5.9% increase seen the prior month.

Heavy-Duty Regional Tractor (HR) values increased 2.1% from October to November, compared to the 6.3% increase seen the prior month.

Heavy-Duty Construction (HC) vales increased 3.8% from October to November, compared to the 9.5% increase seen the prior month.

Medium-Duty Trucks

The chart above illustrates the monthly adjustment trend for Medium Duty trucks.

Production delays mixed with increasing demand on last mile deliveries continue to help improve values for units in this segment.

From October to November, Medium Duty Trucks have increased an overall weighted average of 1.7% compared to the 2.7% increase seen from September to October.

So far this year, Medium Duty values have increased 23.7%. This is amazing considering MD units depreciated 13.1% during the same period in 2020.

According to the Federal Reserve Economic Data (FRED), new retail sales grew 2% from July to August. New retail sales figures of September were reported at 37,004 units. This number is close to the figure reported this time last year, at 38,577 units; however, we are down 22% from the figures reported in September of 2019.

ATA Truck Tonnage improves slightly for August, reporting an increase of 0.5% from July. It’s important to point out though, that these numbers are extremely positive considering the pandemic, supply chain issues, and driver/operator shortages.

Reports are indicating that driver interest is down due to the reduced number of driver applicants and graduates coming out of school. There is also a lack of drivers returning to work due to strong unemployment benefits. Interest will likely increase as time goes on and unemployment benefits are reduced.

With backed-up freight and the Holiday Season just around the corner, we expect to see a continued slow recovery as far as production and transportation go, with continued strengthening of used vehicle prices.

Commercial Trailer Market Update

Commercial Trailer values continue to increase as new production issues are causing scarcity in both new and used inventory.

Wholesale and retail transactions on all trailer segments continue a positive trend as demand continues to rise.

In addition to transportation, some trailers are used as storage. With freight being backed up due to equipment availability or driver shortages, Dry Vans, Refrigerated Vans, and Lowbed trailer demand has surpassed the rest of the pack.

Dry Van values have increased 17.8% for October, compared to the 18.1% increase from Q3.

Dump Trailers were flat this past quarter, showing only a 0.6% increase for Q3.

Refrigerated Vans have gained 14% for October, compared to the 2.8% increase seen during Q3.

Following a slight drop in Q3, we increased Lowbed Trailers 6.6% heading into Q4.

We expect values for all trailer segments to continue increasing as new and used equipment becomes more scarce.

More Dealer Ops

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →

IA American Appoints Two Execs

Senior vice presidents of the company's agent and dealer channels chosen to support general agents and help auto dealers with sales and performance.

Read More →

Cox Automotive Acquires Inspection Firm

Full ownership of Alliance Inspection Management, or AiM, meant to unlock growth for Manheim inspection capabilities

Read More →

Assurant Expands Partnership With Holman

Extended collaboration delivers training, products and performance development to 30 newly acquired Holman dealerships

Read More →

Franchises, Throughput Down in First Half

A handful of states see franchise growth through June, while EV sales per store boost overall business in U.S.

Read More →