Fraud Against Car Dealers Has Never Been More Prevalent

These scams and schemes could impact any dealership’s profits and put their reputations with lenders on the line.

These scams and schemes could impact any dealership’s profits and put their reputations with lenders on the line.

IMAGE: Getty Images

Auto loan fraud in the U.S. is already a big problem, and it continues growing. Point Predictive estimates that approximately $7.8 billion in car sales will be completed and financed with loans containing misrepresentation on the application.

That is a really big number. It’s the highest estimated loss exposure that the industry has faced since Point Predictive began tracking auto loan fraud. And it’s more than double the loss that the industry was exposed to only 10 years ago.

Unfortunately, many car dealers across the U.S. are bearing the brunt of that fraud since some lenders force buybacks after discovering that the loan application contained fraud.

That’s why fraud experts are advising dealerships to detect and prevent fraud schemes involving misrepresentation on the loan application. A dealership’s business could depend on it.

Recovering From Fraud Is Painful and Costly for Dealerships

Recovering from an instance of fraud can be painful for dealerships. Statistically, most U.S. car dealers will source at least one fraudulent loan per year. On average, dealerships can expect one fraudulent loan out of every 200 loan applications that they submit to lenders. Some dealers know this already, but those who don’t should do the math and acknowledge the risk.

One fraudulent loan application out of every 200 might sound like a small number. But consider the extraordinary cost of that fraudulent loan application for the lender. The average funded loan containing fraudulent information, if pushed back to the dealer, represents a loss of at least $21,000. Because the dealer’s portion of the profit on a car is often only a couple thousand dollars, it takes a dealership 10 additional sales to make up for the cost of that fraudulent loan.

Dealers don’t want fraud. The bottom line is that it hurts your business.

Many Ways You Can Be Targeted by Unscrupulous Borrowers and Fraudsters

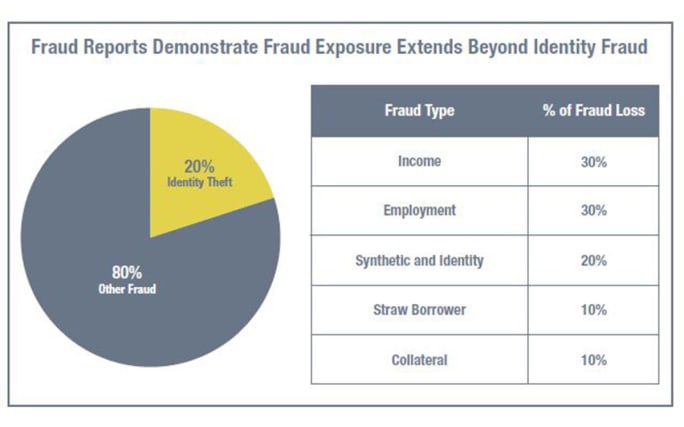

Point Predictive tracked fraud loss exposure across more than 100 million car loans, and we found that dealers are targeted by a plethora of crafty fraud schemes. Interestingly enough, most dealerships only focus on preventing a single type of fraud: identity theft. This narrow focus leaves them exposed to potentially thousands of dollars in risk exposure.

There are five types of fraud that dealerships can be liable for:

Identity fraud. Borrowers provide stolen identities or “create” new synthetic identities to fraudulently finance the vehicle.

Income fraud. Borrowers lie about their income.

Employment fraud. Borrowers lie about where they work, how long they have worked, or even their job title.

Straw borrower fraud. Borrowers act as a front for the real purchaser of the car and then deliver the car to someone else.

Collateral fraud. Finance managers or salespeople report a range of additional options, services, or trim levels on the vehicle that aren’t actually on the vehicle. This is typically done to secure more financing for the applicant than she or he would actually qualify for if the financed amount was lower.

These 5 Rising Fraud Schemes are Causing More and More Losses

The pandemic changed a lot of things in the auto industry. That is particularly true when it comes to fraud. As the behaviors of car shoppers changed, fraudsters adjusted their own behaviors to take advantage. These days, the car buying experience has become a predominantly online, digital transaction, while the time spent in a dealership has been more limited.

Here are the five fraud schemes that dealers need to be aware of:

Fake Employment. The use of fake employers on credit applications has risen 400% since the pandemic began in March of 2020. “Fake” employment is often a service sold to borrowers on the margins of credit eligibility by services offering “credit repair.” These services arm the borrower with forged paystubs and a phone number used for the purposes of fraudulently verifying employment to the lender. Often this phone number actually works, and naturally the individual answering the phone convincingly “confirms” employment as expected.

Over 100 new fake employers are being discovered by Point Predictive’s fraud analysts each week, amounting to millions of dollars in attempted fraud against dealers and lenders.

Stolen, fabricated, and difficult to verify identities are used in fraudulent ways. Identity fraud and creation of synthetic identities is soaring in auto lending. By all accounts more than $1.2 billion in loss exposure will cross lenders’ desks this year. But this year there’s a twist — the fraudsters are using face masks to hide their identities during an in-store interaction, leaving quickly and having cars delivered to them at dead-end locations where they can never be traced.

Straw borrowers are buying cars to covertly sublease them. The pandemic forced many dealerships to temporarily shut down or significantly limit their activity and inventories. At the same time, many rental agencies sold off portions of their fleets. This allowed peer-to-peer platforms such as Turo to thrive. Services like Turo continued to offer renters a diverse selection of vehicles for short-term rental with an elegant customer experience and lower rental rates compared to traditional rental agencies.

But that has also resulted in a sharp spike in straw borrower fraud. Borrowers looking to cash-in are using straw borrowers to help them fraudulently finance vehicles, which are then listed and rented on Turo for profit to the fraudster.

Did we mention paystubs? Some lenders are reporting that up to 40% of the paystubs they receive from some dealerships are forged or altered. But it certainly isn’t a problem limited to shady dealers. On average, even the astute dealership will still receive one fraudulent paystub out of every 12 paystubs submitted by an applicant. Suspicious documentation is becoming far more prevalent, and every dealership needs to protect against it.

5 Ways to Protect Your Dealership from Fraud

Just because fraud has risen dramatically, it doesn’t mean your dealership will be specifically targeted. Even dealerships that protect themselves will need to fight fraud, since the nature of these attacks change quickly. One of the most common ways to be victimized by a new type of fraud is to be effective at preventing older schemes. Here are some ways you can protect your dealership.

Don’t just focus on identity fraud. Identity fraud prevention is important, but it shouldn’t be the sole focus — 80% of buybacks might not be related to identity-related fraud scams.

Always check to see that the income makes sense for what you know about the applicant. Look for red flags for potential income fraud. An applicant who claims to be employed in a low-wage position should prove income that aligns with that position. Younger applicants should rarely claim income that is typical of a mid- or late-career employee. Finally, an applicant who is making a dramatic leap in the cost of their cars, such as trading in a junker for a newer model luxury or high-end vehicle should be verified to assuage the suspicion of fraud.

Check employment discrepancies. Oftentimes a bogus paystub will have mathematical inconsistencies that become apparent upon detailed inspection. Values on the stub might not add up correctly. Bonuses, commissions, and withholdings may look distorted relative to the wages claimed. Pro tip: you can always ask an applicant to sign an IRS Form 4506T, which gives you permission to verify income that the applicant reported to the IRS.

Beware of straw borrowers. Look for potential straw borrower red flags. Straw borrowers are often coached by a co-conspirator, and certain questions, requests, and actions might not make sense.

Monitor new finance managers. If a new finance manager’s performance is too good to be true, it might not be true. F&I managers who seem able to work miracles to get even the most down and out borrower funded might be doing something extra to get those loans approved. It is crucial to monitor the process, enforce intentional risk controls, and make sure that new finance managers are keeping the dealership’s business and reputation in top shape with its lender network.

Like many challenges facing the car buying market, the problem of fraud will never go away. We expect it to continue to grow and become even more challenging to prevent. Dealers must leverage every practical tool and technology to keep fraud at bay.

Frank McKenna is the co-founder and chief fraud strategist for Point Predictive. Frank is a recognized and respected expert who has helped thousands of institutions reduce fraud loss and better manage risk.

More Compliance

RockED Offers Free FTC Pricing Education Series for Dealerships

The program is designed to help dealers, managers and front-line teams get more information about Federal Trade Commission pricing enforcement, advertising transparency and evolving regulation.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

AAMS Training and Mosaic Compliance Services Merge

The strategic combination is intended to expand technology-driven compliance solutions for the automotive industry.

Read More →

The Jurisprudence of Pricing

Legal concept helps makes sense of California’s recently passed version of the failed federal CARS legislation.

Read More →

Trump 2.0 and Enforcement Priorities

The upshot is don’t relax, because regulation indeed continues.

Read More →

June Is Automotive Service Professionals Month

Observance is opportunity to thank technicians for their crucial role in auto retail.

Read More →

Cox Automotive Releases Compliance Guide

New edition walks auto dealers through relevant regulations for 2025.

Read More →

Trump 2.0 and Retail Automotive

Administration’s plans should generally bode well for the industry.

Read More →

CARS Rule Update: 5th Circuit Oral Arguments Recap

In this video, Jim Ganther of Mosaic Compliance Services, recaps the key takeaways from the oral arguments in the critical CARS Rule case, including potential outcomes and what dealers should do to stay ahead of compliance changes.

Read More →

State of the CARS Rule, Part 3

The players in the automotive industry should coordinate their responses to this pending regulation.

Read More →