Residual Value Risk Transitioning to Electric Vehicles — Will History Repeat Itself?

The transition to EVs is not a matter of if, but a matter of when, and the industry must pay attention to the impacts of the potentially imminent and rapid transition from ICE vehicles to EVs.

The transition to EVs is not a matter of if, but a matter of when, and the industry must pay attention to the impacts of the potentially imminent and rapid transition from ICE vehicles to EVs.

IMAGE: Getty Images

The transition from internal combustion engine vehicles to electric vehicles started back in 2017, a banner year for EVs. That year, new electric vehicle (EV) sales surpassed one million units globally. Many countries announced their timetables to end the internal combustion engine (ICE) age in the automotive industry, and manufacturers announced plans to introduce many EV models. Despite the excitement generated at auto shows and by the media, there were still significant technological hurdles to overcome. For example, the cost of batteries was too high, creating a significant differential in the total cost of ownership for an EV when compared to an ICE vehicle. Public charging stations were hard to locate, and charging took far too long when compared to several minutes to fill up with gas.

These differences created great uncertainty as to whether EVs could ever replace ICE vehicles. Despite the government and industry pledges to support EVs over the long term, the EV initiative was doomed to fail unless the industry could achieve large reductions in battery costs and overcome technical hurdles.

Fast forward four years, and 2021 is shaping up to be another banner year for EVs. Battery costs are coming down faster than most projections. Many EV startups are now firmly established (e.g., Tesla and NIO) in terms of both vehicle sales and market cap. EV sales are expected to exceed 2 million units in China alone in 2021. The transition to EVs is not a matter of if, only a matter of when. The industry is now seriously concerned about the impacts of the potentially imminent and rapid transition from ICE vehicles to EVs.

One of the impacts of the transition from ICE vehicles to EVs is on the residual value of lease portfolio. In the past few years, EV residual values have been improving along with their driving range. On the other hand, the residual values of ICE vehicles have not yet been impacted by the competition from EVs. This will likely change over the next few years as further improvement in EVs make them superior products compared to ICE vehicles in terms of both driving experience and total cost of ownership. In other words, EVs could become the preferred vehicle to drive. When this happens, the market share of EVs will increase rapidly and ICE vehicles, now inferior substitutes, will likely have lower residual values.

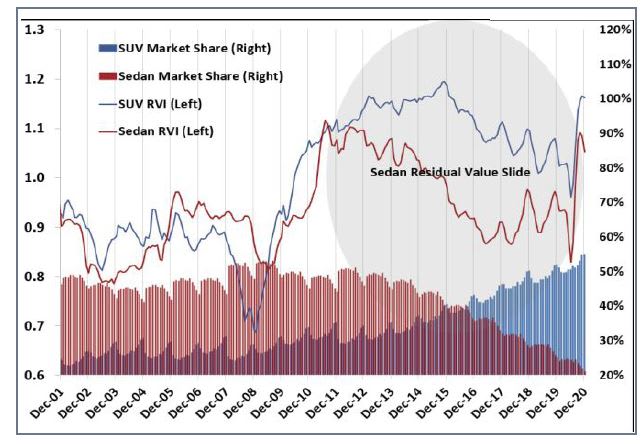

We have observed the impact on residual values when auto market shifted from sedans to SUVs. As we can see in the figure below, after the 2008 recession, SUVs (including crossovers) became extremely popular with market share increasing consistently from 26% in 2008 to 52% in 2020. During the same period, we saw the residual values of these two vehicle types diverge and the gap in values between sedans and SUVs grow as large as 20%. Lessors with portfolios heavily concentrated in sedans suffered large residual value losses.

When consumers switch from ICE vehicles to EVs in large scale, the negative impact can be more dramatic than the decrease in values that sedans experienced in the past 10 years. The residual value slide for sedans shown in the chart is a gradual downturn compared to the cliff that ICE vehicles may fall over if the transition to EVs turns out to be a swift process. This ICE cliff will be the result of a combination of consumer preference shift, EV cost reduction, and changes in refueling networks. While the charging stations will become ubiquitous, the number of gasoline stations will start to decrease as sales of new ICE vehicles decrease. No one can predict when and how quickly this will happen, but few people still question that this transition will happen.

On a given day, there is about $200 billion in residual values associated with the 8-10 million leased vehicles on the books of all lessors in the U.S. A 10% downturn in residual values results in a $20 billion residual value loss. The financial impact of this residual value downturn is enormous. Insurance companies helped the auto industry manage residual value risk in the past. In China, where electric vehicles are further developed, insurance companies are working with manufacturers to design creative auto finance products using residual value insurance. In the U.S., insurance companies can also help the auto industry manage its residual value risk as they did during the early days of auto leasing business.

Wei Fan is senior vice president, head of passenger vehicle and analytical services for RVI Group, a provider of residual value insurance, financial solutions and analytical services.

More Dealer Ops

Dealer Debrief: Defection Data & EV Updates

In this week's debrief, host Lauren Lawrence discusses how to use defection data to your advantage and the latest on EV sales and charging infrastructure.

Read More →

How Defection Data is Bridging the Dealership Conversion Gap

Lead volume is flat, cross-shopping is up and brand loyalty is in retreat. As confident sales teams keep losing buyers they thought they had, daily industry sales data is showing dealers exactly where their funnel is breaking and how to fix it without buying a single new lead.

Read More →

Dealer Debrief: Where are you losing customers?

In this week's debrief, host Lauren Lawrence discusses the hidden leaks in dealerships where you might be losing customers without even realizing it.

Read More →

Dealer Debrief: Improving Your Inventory Management

In this week's debrief, host Lauren Lawrence covers a new survey that shows what service technicians really want and two launches that could help improve your inventory and vehicle life cycle management.

Read More →

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

What Market Timing Mistakes Mean for Your Reinsurance Program

When volatility hits, dealer-owned reinsurance programs face a familiar temptation: pull back and wait for calmer waters. New data from BOK Financial shows why that instinct can quietly cost you years of surplus growth.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →