Black Book: Weekly Market Report

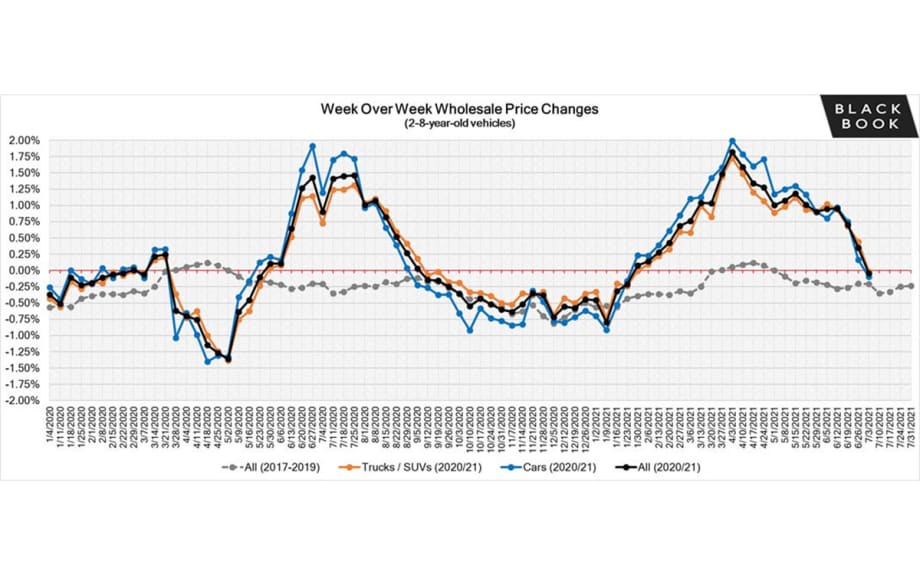

Wholesale values are finally starting to simmer down but make no mistake, supply channels haven’t been restored and the market remains strong.

Wholesale values are finally starting to simmer down but make no mistake, supply channels haven’t been restored and the market remains strong.

IMAGE: Black Book

Wholesale Prices, Week Ending July 3rd

Wholesale values are finally starting to simmer down but make no mistake, supply channels haven’t been restored and the market remains strong. The rate of positive-adjustment decreased throughout June, resulting in the first overall weekly decline since mid-January!

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.10% +0.17% -0.30%

Truck & SUV segments -0.02% +0.44% -0.15%

Market -0.04% +0.35% -0.21%

Car Segments

On a volume-weighted basis, the overall Car segment decreased –0.1%.

For reference, the previous week increased by +0.17%.

Sub-compact segment had the strongest weekly gain at +0.7%.

Compact car segment had the steepest decrease at -0.49%

Five of the nine segments declined this week

Truck / SUV Segments

On a volume-weighted basis, the overall Truck segment decreased -0.02% this past week.

For reference, the previous week increased by +0.44%

Full-size Van segment had the strongest weekly gain at +0.92%.

Small Pickups had the steepest decrease at –0.48%

Six of the thirteen segments declined this week.

Newer Used Vehicles (0-2-year-old)

Driven by an extreme shortage of rental returns and limited inventory of new vehicles, the prices of newer used vehicles have been experiencing large weekly gains in the Spring. While wholesale prices are exceeding MSRP in some cases, the rate of increase has started to slow down in the last several weeks and the market was essentially flat last week.

The table below shows the average weekly price changes for 0-2-year-old vehicles.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -0.05% +0.12% -0.28%

Truck & SUV segments +0.04% +0.43% -0.15%

Market +0.01% +0.35% -0.19%

Weekly Wholesale Index

Calendar year 2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 has not had typical seasonality patterns as the market continues to have rapid increases in wholesale values. As we start July, wholesale prices are stabilizing and are around 37% higher compared to the beginning of the year (adjusted for the mix).

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year.

Retail (Used and New) Insights

General Motors, Ford Motor Co., and Stellantis announced that they will eliminate mask mandate for fully vaccinated workers at their U.S. factories beginning July 12.

Self-driving startup, Zoox Inc., who is owned by Amazon, recently released a safety report with details about nine proprietary safety features not found in conventional vehicles including rider protection in the vehicle.

Jaguar is looking for a new platform for their future EV lineup after cancelling plans for an all-electric remake of their XJ sedan

In coming months, Bugatti is expected to transition as part of a joint venture with Croatian electric-car maker Rimac and Porsche.

BMW confirmed that the i3 will be discontinued in the U.S. market – production is scheduled to end in July of this year.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices for the last several weeks of 2020. As demand rebounded, retail prices have lagged slightly behind wholesale prices, but March had an accelerated growth in retail prices. In April and May, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. As June came to an end, retail prices continued to increase. Currently, retail prices are more than 24% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles.

Inventory

Used Retail

Current used retail listing volume is about 10% below the start of the year. The inventory levels have been slowly but consistently increasing over the last three months, as we start to see some softening of retail demand.

Days-to-turn has continued to decrease since the middle of March as sourcing both new and used inventory continues to be a challenge; it now stands around 32 days, which as the graph below shows, is lower than we have seen in the recent past.

Wholesale

As floor pricing remains strong and the availability of average and clean vehicles remains scarce, conversion rates have started to slow down. Average sell rate now sits around 70% and has hovered in the low 70% range since April.

Despite the limited inventory on dealer lots, dealer lanes continue to have higher volume at auction, while manufacturers’ remarketing lanes are offering less and less in open sales channels. Dealers have found creative ways to diversify their source of inventory, and their innovation seems to be paying off.

OEM remarketers are able to continue raising floors in the lanes for cleaner vehicles because of an extremely limited inventory pipeline. Because of the scarcity in the wholesale market, even vehicles with slight damages or open recalls are bringing top dollar.

Originally posted on F&I and Showroom

More Dealer Ops

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →

IA American Appoints Two Execs

Senior vice presidents of the company's agent and dealer channels chosen to support general agents and help auto dealers with sales and performance.

Read More →

Cox Automotive Acquires Inspection Firm

Full ownership of Alliance Inspection Management, or AiM, meant to unlock growth for Manheim inspection capabilities

Read More →

Assurant Expands Partnership With Holman

Extended collaboration delivers training, products and performance development to 30 newly acquired Holman dealerships

Read More →

Franchises, Throughput Down in First Half

A handful of states see franchise growth through June, while EV sales per store boost overall business in U.S.

Read More →