Black Book: Weekly Market Update

With the large declines in the market, buyers are being more hesitant to pay any extra money for inventory.

Wholesale Prices, Week Ending August 19

The wholesale market continued to experience record declines for a third consecutive week, prices in some mainstream segments decreasing by more than 2%. On the other hand, we have yet to see any meaningful decrease in used-retail listed prices.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -1.73% -1.35% -0.19%

Truck & SUV segments -1.43% -1.49% -0.21%

Market -1.52% -1.45% -0.21%

Car Segments

On a volume-weighted basis, the overall car segment decreased 1.73%. For reference, in the previous week, cars decreased by 1.35%. The decline exceeds the largest single-week depreciation experienced at the onset of the pandemic of 1.40%.

The 0- to 2-year-old car segments were down 1.20%, and 8- to 16-year-old cars declined 1.90%.

All nine car segments decreased, seven reporting declines exceeding 1%.

Compact (-2.51%), midsize (-2.16%), and full size (-2.15%) cars declined more than 2%, the third straight week of single-week depreciation exceeding 2% in the segment.

Premium sporty and prestige luxury continue to experience typical seasonal depreciation.

Truck / SUV Segments

The volume-weighted overall truck segment decreased 1.43%, which is consistent with depreciation the prior week, of 1.49%.

The 0- to 2-year-old models declined 1.20%, while the 8- to 16-year-olds declined 1.10%.

All 13 truck segments declined, and 11 had declines greater than 1%.

Minivan (-2.15%) was the only truck segment to drop by more than 2%. Despite being a large decline, it's still less than some of the declines last year and at the onset of the pandemic that were as large as 2.50%.

The small pickup (-0.74%) segment had smaller depreciation than the larger full-size pickup segment (-1.34%).

Weekly Wholesale Index

The graphic below looks at trends in wholesale prices of 2- to 6-year-old vehicles indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Used Retail Prices

Used-retail prices are more accessible than in years pas due to the proliferation of no-haggle pricing for used-vehicle retailing. Transparent pricing upfront makes the car-buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.

At the onset of the pandemic, in CY2020, used-retail prices increased slightly, following typical seasonal patterns, then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, they increased as supply of new-vehicle inventory started to become scarce, but retail demand slowed at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March 2021 started the dramatic increases in prices, fueled by stimulus payments, tax season and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up again to start the fourth quarter, when they steadily increased. As CY2021 came to an end, the retail listing price index closed 36% above where the year began, then remained relatively stagnant through most of CY2022. In the fourth quarter, the Retail Listings Price Index started to decline but not as steeply as the wholesale price index.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graphic below looks at 2- to 6-year-old vehicles. The index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

The Used Retail Active Listing Volume Index currently sits at 1.02 points.

The used retail days-to-turn estimate is currently hovering above 51.

Wholesale

For the third week in a row, the market had steep declines in both the car and truck segments. Auction conversion rates declined 1% after the prior two weeks showed improvement in the market. With the large declines in the market, we are now seeing buyers being more hesitant to pay any extra money for inventory. Buyers and sellers are both in a wait-and-see mode.

As always, the Black Book team of analysts will keep their eyes on the market, watching for developing trends and insights.

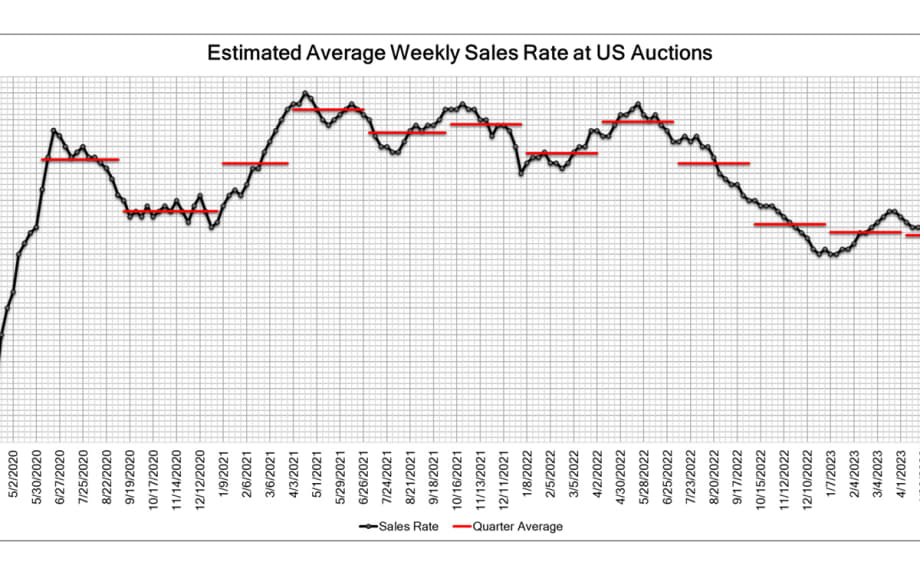

The estimated Average Weekly Sales Rate declined to 49%.

More Dealer Ops

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →

IA American Appoints Two Execs

Senior vice presidents of the company's agent and dealer channels chosen to support general agents and help auto dealers with sales and performance.

Read More →

Cox Automotive Acquires Inspection Firm

Full ownership of Alliance Inspection Management, or AiM, meant to unlock growth for Manheim inspection capabilities

Read More →

Assurant Expands Partnership With Holman

Extended collaboration delivers training, products and performance development to 30 newly acquired Holman dealerships

Read More →

Franchises, Throughput Down in First Half

A handful of states see franchise growth through June, while EV sales per store boost overall business in U.S.

Read More →