NY Fed: Household Debt Surpasses 2008 Peak in Q1

The feat comes almost nine years after the Great Recession, when household debt reached $12.68 trillion. But the debt and its borrowers look quite different today, the New York Fed noted, and auto finance sources showed signs of tightening in response to some deterioration in auto loan performance.

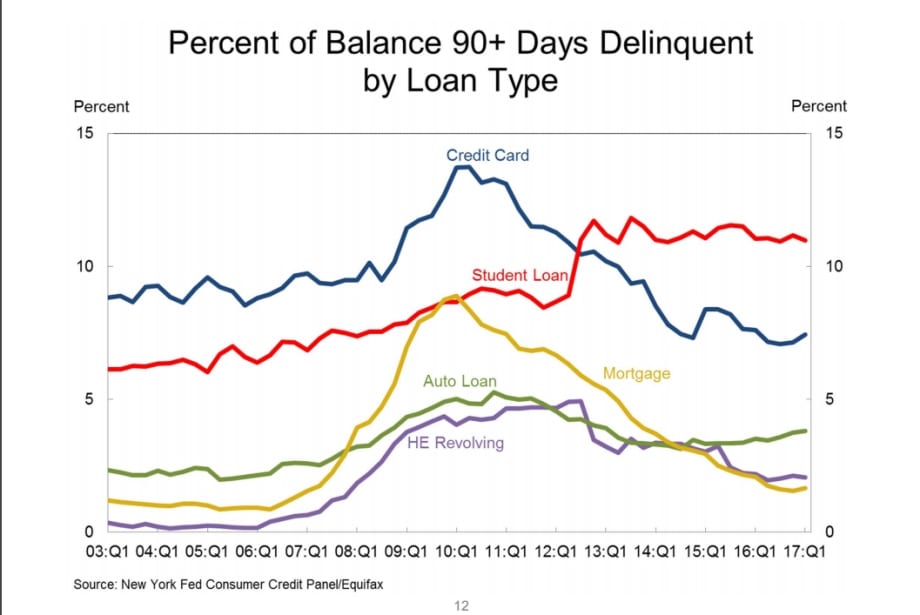

NEW YORK – Total household debt in the first quarter finally surpassed its $12.68 trillion peak reached during the 2008 Great Recession, the Federal Reserve Bank of New York reported this week. And it happened during a period that saw a notable uptick in credit card debt transitioning into delinquencies, and a continued upward trend of auto loans transitioning into serious delinquencies.

Student loan transitions into serous delinquencies remained high, the New York Fed noted.

As of March 31, household debt reached $12.73 trillion, a $149 billion increase from the fourth quarter of 2016 and the 11 consecutive quarterly increase. And according to the New York Fed’s quarterly report, overall household debt is now 14.1% above the second quarter 2013’s trough.

“Almost nine years later, household debt has finally exceeded its 2008 peak, but the debt and its borrowers look quite different today,” said Donghoon Lee, research officer for the New York Fed. “The record debt level is neither a reason to celebrate nor a cause for alarm. But it does provide an opportune moment to consider debt performance.”

Aggregate delinquency rates were roughly flat in the first quarter, with some variations across product types. And as of March 31, 4.8% of outstanding debt was in some stage of delinquency. Of the $615 billion of debt that was delinquent, $426 billion was labeled seriously delinquent (at least 90 days late).

Auto loan balances increased by $10 billion during the quarter. Auto loan delinquencies were flat, with 3.8% of auto loan balances 90 or more days delinquent on March 31. But auto finance sources responded to the slight deterioration in auto loan performance.

Auto loan originations totaled $132 billion during the period, a decline from the prior quarter but a but an uptick from the same period last year. However, the period saw a tightening in underwriting guidelines, with the median score for originating auto loan borrowers ticking up to 706.

Looking at credit scores for both auto loan and mortgage originations, the New York Fed noted that origination volumes to borrowers with credit scores under 660 shrank since the same quarter last year, while origination volumes with credit score above 720 have increased considerably.

“While most delinquency flows have improved markedly since the Great Recession and remain low overall, there are divergent trends among debt types,” Lee noted. “Auto loan and credit card delinquency flows are now trending upwards, and those for student loans remain stubbornly high, hovering around 10% at an annual rate over the past five years.”

In an accompanying blog co-written by Lee, the New York Fed noted household debt picture is vastly different than in 2008. Mortgages now have a much smaller share than in 2008, while auto and student loans have increased in their share.

“Balances are increasingly shifting toward more creditworthy and older borrowers,” the blog reads, in part. “These shifts in borrowing patters and characteristics of borrowers, paired with the long economic recovery and a strong labor market, have resulted in very low delinquency rates for most types of debts except for student loans.

“More recently, performance on mortgages have continued to improve, while auto loan delinquency flows have been trending upward since 2012,” the blog continues. “Credti card transitions have also ticked up. The standout, however, has been student loans — with new serious delinquency flows that deteriorated steadily between 2004 and 2014 and have remained stubbornly high since.”

Originally posted on F&I and Showroom

More Dealer Ops

Dealer Debrief: Defection Data & EV Updates

In this week's debrief, host Lauren Lawrence discusses how to use defection data to your advantage and the latest on EV sales and charging infrastructure.

Read More →

How Defection Data is Bridging the Dealership Conversion Gap

Lead volume is flat, cross-shopping is up and brand loyalty is in retreat. As confident sales teams keep losing buyers they thought they had, daily industry sales data is showing dealers exactly where their funnel is breaking and how to fix it without buying a single new lead.

Read More →

Dealer Debrief: Where are you losing customers?

In this week's debrief, host Lauren Lawrence discusses the hidden leaks in dealerships where you might be losing customers without even realizing it.

Read More →

Dealer Debrief: Improving Your Inventory Management

In this week's debrief, host Lauren Lawrence covers a new survey that shows what service technicians really want and two launches that could help improve your inventory and vehicle life cycle management.

Read More →

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

What Market Timing Mistakes Mean for Your Reinsurance Program

When volatility hits, dealer-owned reinsurance programs face a familiar temptation: pull back and wait for calmer waters. New data from BOK Financial shows why that instinct can quietly cost you years of surplus growth.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →