Season of Prosperity

This year’s Special Finance Benchmarks prove the subprime auto finance market continued to sizzle throughout the summer of 2014.

Every year since 2002, it has been my job to collect and analyze the thousands of transactions which comprise the annual Special Finance Benchmarks. The report we released at this year’s Industry Summit, held in September at Paris Las Vegas, was our most ambitious yet. More data means more useful numbers, better education and a heck of a lot more work, and I am grateful to the staff here at DealerStrong for their help.

This year, for the first time, we merged our database with that of ProMax Unlimited, a system dealers use to pull credit and deliver vehicles. Fueled by an additional 165,000 transactions covering May, June and July 2014, we were able to add several statistically relevant standards.

Inside the Numbers

The benchmarks are calculated from the 75th percentile of all deals, not the “average” 50th percentile. By definition, one in four deals are greater than benchmark and three in four fall below. While we are not publishing averages, let it be stated that the benchmark deals are approximately $1,200 greater than an average total deal gross profit.

As a result, for 2014, you will notice many changes. First, gone are the separate benchmarks for franchised and independent dealers. As the numbers were analyzed, it became clear that new- and used-vehicle sales offered a better distinction.

Perhaps the most noticeable change is the absence of “the number.” I refer, of course, to the total deal gross profit that many dealers want to multiply by their anticipated volume. Instead, in the table on Page 32, you will see that we now have gross profits defined by the five subprime credit tiers, for both new and used.

The full report, available at www.dealerstrong.com, ranks the auto finance companies serving each tier by new and used volume. You can see what the 75th percentile transaction for deals in each tier actually look like, including sale price, true down payment and average credit score. Note that the highest volume finance company in a tier may not necessarily have the highest gross profits. Dealers may choose them more often due to the states in which they operate, programs that match their inventories or excellent service.

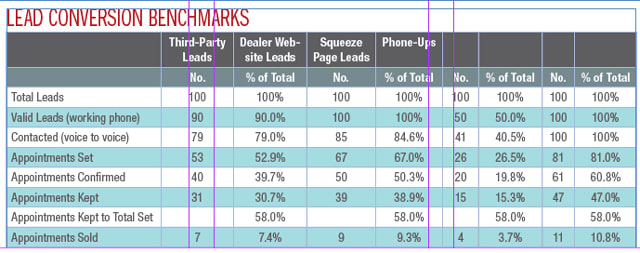

Finally, the phone/BDC and sales activities were expanded to include dealer website “squeeze page” lead performance metrics. Please note that this particular benchmark is based on raw leads, from which a high percentage are eliminated as not having valid or working phone numbers.

From all this analysis came some pretty interesting facts. Here are just a few highlights:

47% of the transactions analyzed had prime credit scores (680+). Nearly 20% had nonprime credit (621+). That means one-third of all sales had credit scores of 620 and below.

Used-vehicle sales still make up nearly 85% of all special finance sales.

57.4% of all used vehicles financed were SF credit tiers. Experian says the average credit score for someone financing a used car is 655.

The vehicle gross profits (“front-end”) for new vehicles are shown to be substantially lower than used vehicles. Most dealers do not include factory stair-step incentives, so you should add back approximately $700 to the vehicle gross profits for new cars.

Monthly payments (payment-to-income ratios) are still important, especially for used vehicles. Only one credit tier had average monthly payments of more than $400 for used-vehicle transactions, and that was Tier 1 ($409). To be a top performer, you must keep the average of your monthly payments below $400.

Captive finance companies enjoy OEM support and are much less concerned about monthly payments on new vehicles sold in SF. The average captive transaction inflates the payment by more than $100, even for Tier 4, where the average payment is a whopping $555.

If you are a franchised dealer and question whether you should show a SF customer a new or a used vehicle, make that decision — after analyzing credit and the bureau — on income. There was a $168 difference in average monthly payments between a new and used vehicle in SF Tier 4.

The “No Score” SF tier is much more significant than I imagined. It includes true first-time buyers, undocumented residents, and so-called credit criminals. This market is nearly 40% as big as the largest tier, SF Tier 2, and has equal penetration for new as used. Affordability is key: Average monthly payments were $348 for used and $418 for new.

The great American myth that you can’t make any money in F&I is once again debunked. The benchmark for SF deals across all tiers is $1,093 for used and $1,154 for new, both up from 2013.

Capital One Auto Finance ranks in the Top Four of every SF tier.

Credit Acceptance Corp. has always had significant market share among the bottom used vehicle SF credit tiers. Now, that company is making serious waves in SF Tier 2, where it ranks among the Top 10 in volume and has the second highest at-time-of-sale gross profit at $4,126 among benchmark deals.

The only area of the transaction data not fully developed is that of SF Tier 4 for used vehicles. Since the data is pulled from DealerStrong and ProMax dealers, many smaller independent dealers are not included in this data. Westlake Financial doesn’t appear anywhere in the volume mix for benchmark dealers even though they are funding more than 10,000 deals per month. Their transactional data is accurate, as they still have significant volume reported, but not enough to show up in the Top 10 in volume in SF Tier 4.

If I had to guess, I would estimate that, in reality, SF Tier 4 (used vehicles) is likely the size of SF Tier 3, as there are a number of other local and regional companies serving smaller independent dealers in that tier.

Don’t forget credit unions! No single credit union has more than a 1% national market share, but their combined presence is a force. You should investigate all credit unions available in your market as they often have unique solutions for SF customers.

Finally, when examining phone and sales activities, even with more dealers creating BDCs to serve SF, proficiency levels seem to be dropping in general.

So there you have my observations on the 2014 Special Finance Benchmarks. You can find all the reports at www.dealerstrong.com, and please feel free to email me with any questions. Until next month, great selling!

Greg Goebel is the CEO of DealerStrong and the industry’s leading special finance trainer since 1989. He is an 18-year former dealer principal and a highly sought-after speaker, author and consultant. GGoebel@AutoDealerMonthly.com

More Dealer Ops

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

Timing the Market Can Hurt Long-Term Program Performance

For dealer-owned reinsurance entities, avoiding volatility entirely can mean falling behind inflation and missing market rebounds that drive long term surplus growth. Missing just a handful of strong market days can materially impact cumulative returns—an important reminder for long horizon trust and investment strategies.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →

IA American Appoints Two Execs

Senior vice presidents of the company's agent and dealer channels chosen to support general agents and help auto dealers with sales and performance.

Read More →

Cox Automotive Acquires Inspection Firm

Full ownership of Alliance Inspection Management, or AiM, meant to unlock growth for Manheim inspection capabilities

Read More →

Assurant Expands Partnership With Holman

Extended collaboration delivers training, products and performance development to 30 newly acquired Holman dealerships

Read More →

Franchises, Throughput Down in First Half

A handful of states see franchise growth through June, while EV sales per store boost overall business in U.S.

Read More →