COVID-19 Market Update

Black Book has released a COVID-19 market update.

Black Book has released a COVID-19 market update.

Image provided by Black Book

BLACK BOOK – Today, Black Book released a COVID-19 market update.

As we enter the last week of June, federal stimulus, together with still limited used vehicle inventory, helped to maintain the strength of wholesale prices across almost all vehicle segments, with volume-weighted overall car and truck segments both showing gains for the fifth week in a row, increasing 1.43% overall – the highest weekly appreciation in recent history. As for specifics, the overall car segments increased by 1.91% (compared to 1.54% the prior week) and the overall trucks and SUV segments increased again this past week at 1.15% (compared to 1.11% the prior week).

Although prices have remained strong over the last several weeks (and reached pre-COVID-19 heights during the last week), on a year-over-year basis, we are still below 2019 levels. A deeper dive into the data reveals that raw prices are indeed higher this year, but the mix of vehicles in the marketplace is different: this year we see cleaner vehicles with significantly lower mileage (3,000 to 6,000 miles less compared to the same three-year-old vehicle a year ago on many popular three-year-old models) hitting the wholesale market. When adjusted for condition and mileage (a true apples-to-apples comparison), June’s prices are about 3% below 2019.

Auction sales volume has returned to pre-COVID-19 levels, with most auctions still operating in a digital only environment. Two weeks ago, we received word that a limited number of Manheim operating locations were going to allow sellers to represent their vehicles on the block during a pilot period. These Digital Block sales offer in-lane bidding with a live auctioneer, however vehicles do not run through the lanes. Over the last few days there was an update from Manheim that the Florida locations that were set to take part in this pilot will have these Digital Block sales postponed, as Florida has emerged as one of the areas in the country where newly confirmed COVID-19 cases are back on the rise. At the same time, we hear that ADESA is making their own plans to start a similar pilot set to launch shortly. These changes at large auction houses come on the heels of the successes being achieved by independent and smaller auction chains who opened back up to in-lane sales over the last few weeks. Demand has been high and dealer attendance, both in person and online, has been significant at these independent auctions, with many achieving above average sales volume and retention. Buyers have been vocal about their desire to attend these sales in person, adding to the pressure received from the large auction houses.

Although we see some recovery in rental demand (outside of airport business), we measured a substantial increase (compared to previous weeks and compared to last year) in volume of rental units sold, as rental fleet companies are beginning to de-fleet and reduce their fleets to match much weaker consumer and business traveler demand. As the supply continues to grow, we are concerned with the throughput at major auctions, as they continue to operate with reduced staff, and with the direct to dealer channel, as there is shortage of personnel too. In our continuous conversations with management teams from major auction chains, they report that they are trying to execute on the increased volume and customer demand without immediately bringing back significant amounts of furloughed staff. There is a concern that this uptick may be short-lived and the need for increased staff may be temporary.

Since the beginning of April, weekly initial unemployment claims remained at record levels. Last week, the Labor Department reported that the US added 1.48 million new jobless claims. The US unemployment rate in April was 14.7%, the highest monthly rate since the Great Depression. In a surprise to many economists, May unemployment decreased to 13.3% due to the success of the Federal Paycheck Protection Program (PPP) and other stimulus measures. The Labor Bureau also noted in its report that there was a classification error in its survey, and the real unemployment numbers should be about three percentage points higher for both April and May. There is also concern that without further Federal stimulus, these gains will be temporary and employment numbers may deteriorate once PPP expires.

With a weakening of the economy and the increase of new COVID-19 cases across the South, consumer confidence remains low. The University of Michigan’s Monthly Consumer Sentiment Index in February was 101 points. As the COVID-19 pandemic spread across US, the index dropped to 71.8 points in April and slightly increased to 72.3 points in May. During recent testimony by Federal Reserve Chair Jerome Powell, he noted that during the months of April and May, “stimulus checks and unemployment benefits are supporting household incomes and spending.” With this one-time stimulus payments and extended unemployment benefits helping the economy, the index for June increased further to 78.1. The gains were not uniform across the country: with the significant reduction of COVID-19 cases, the Northeast region led the way with a record 19.1 points month-over-month jump, while the Southern region rose just 0.5 points due to the dangerous increase in numbers of new infections and fear of further shutdowns.

As more economic data for the second quarter of 2020 arrives, “the GDPNow model [from the Federal Reserve] estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2020 was -46.6 percent on June 25th.”

The overall weakening of the economy is causing demand for vehicle purchases to decline. In addition, gasoline prices reversed the May trend, and started to increase, up $0.36 since the lowest point at end of April to $2.13 per gallon last week, according to the U.S. Energy Information Administration.

At the same time, we expect a large, incremental influx of used inventory to hit the marketplace over the next six months, coming from prolonged lease return delays and downsizing of rental fleets (including the expected sell-off of a large number of Hertz’s units). In addition, lenders expect a significant increase in delinquencies and repossessions in the upcoming months as economy goes through high unemployment. The number of accounts in ‘hardships’ jumped substantially in April and May across all risk groups according to the Monthly Industry Snapshot by TransUnion: about 7% of all accounts were in hardship in May (double the April numbers and 18 times higher than a year ago). The number of ‘hardships’ increased across all risk tiers.

Due to these factors, we expect both wholesale and retail prices to deteriorate later in the summer. On the other hand, due to better than expected (but still very high) unemployment numbers, it is possible that the automotive industry will avoid a more catastrophic economic scenario (severe prolonged recession) that was considered as one of the scenarios in our residual value projections.

Although the economic effects of the pandemic will continue to be felt as far out as three years from now, we still project that wholesale values will return to the pre-COVID-19 baseline by 2023. Used supply will decline due to cuts in retail and fleet sales throughout 2020 and into 2021.

Current Wholesale Market Overview

Auction Insights

Sales this past week continued to be abundant and values are still increasing, as the lack of inventory on dealer lots had them actively bidding in an effort to secure vehicles.

At most of the independent auctions that are having physical sales, we are seeing higher sales conversions, as the desire to be on the physical lane during sale time is still a big draw for many dealers.

Two weeks ago, Manheim announced it would be starting a pilot program to move a selection of simulcast-only sales to Digital Block sales, but due to the increase in COVID-19 cases in Florida the pilot program for those locations in the state have been postponed to the week of July 13th.

There is a new option on the horizon for dealers to source inventory and it comes in the form of a partnership that was announced this past week between Carvana and Manheim with a new wholesale platform, CarvanaAccess.com.

We are also seeing the emergence of alternative wholesale channels for dealers to source inventory from both dealer to dealer platforms and private sellers including The Appraisal Lane, Drivably, DealersLink and Boost Acquisition, amongst others. These newer platforms, while not auction/bidding based in nature, join more established digital auctions platforms like Trade Rev, ACV Auctions, Manheim Express and others who aim to provide inventory options for dealers in need.

Auction Volume

Despite most auctions continuing to operate under an all-digital platform, sales volume has rebounded to a level consistent with, and on some days higher, than this time last year. This is being driven by strong retail sales, which are then leading dealers to use auctions as their main source of inventory. The number of sales bottomed out around an 80% year-over-year decline when most auctions closed their physical sales (and some closed entirely) at the end of March. The graph below illustrates the estimated year-over-year change in sales volume of the wholesale market.

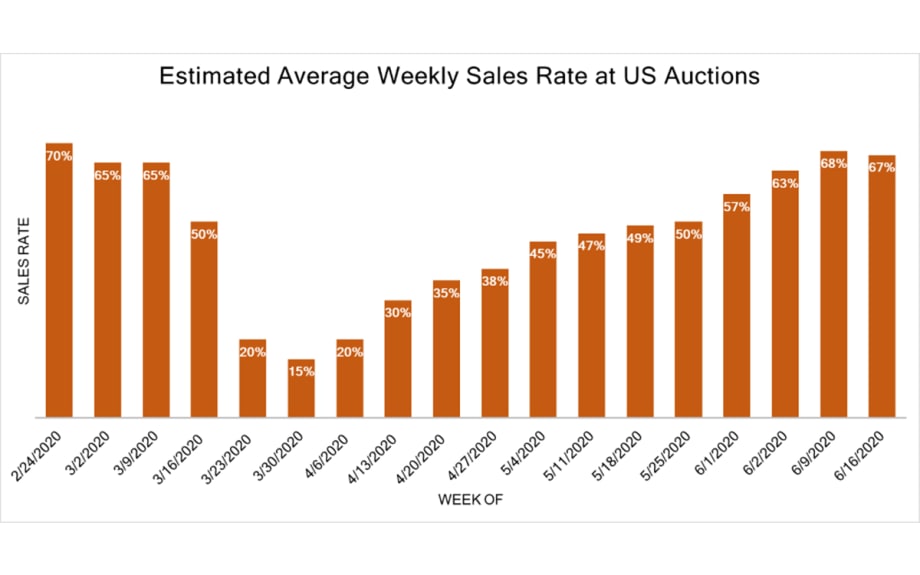

Sales Rate

At the onset of the pandemic, as shelter-in-place orders went into effect, sales rates quickly tumbled into the teens, but rates have been climbing each week and have now stabilized into a percentage that is typical of a springtime market. Black Book’s estimate of the Weekly Average Sales rate is presented below.

Current Wholesale Price Trends

Current Market Level View

Volume-weighted, overall car segment values increased 1.91% this past week. All car segments experienced increases, with the most notable increase being the Sporty Car segment with a gain of 2.45%. The Prestige Luxury Car segment was the only segment to have an increase of less than 1.0% this past week. However, it is still notable as this is a segment that rarely increases. When volume-weighting is applied, the overall Truck segment (including pickups, SUVs, and vans) values increased by 1.15% last week with all segments increasing except Full-Size Vans. Sub-Compact Crossover and Sub-Compact Luxury Crossover segments led the increases for the Truck/SUV segments at 2.53% and 2.52%. These segments have been slower to rebound compared to the larger Compact Crossover segment.

The graph below shows week-over-week depreciation rates for the entire market, including Cars and Trucks / SUVs / Vans for the last several months. Last week, the overall market appreciated by 1.43%. We have now experienced five weeks of overall market rebounding with consistent week-over-week increases in almost all segments.

Year-Over-Year View on Wholesale Prices

The graph above compares Black Book’s Seasonally Adjusted Retention Index for 2019 and 2020 calendar years. The Black Book Used Vehicle Retention Index is calculated using Black Book’s published Wholesale Average value on two- to six-year-old used vehicles, as a percent of original typically-equipped MSRP. It is weighted based on registration volume and adjusted for seasonality, vehicle age, mileage, and condition. The Index offers an accurate, representative, and unbiased view of the strength of used vehicle market values. It measures an ‘apples-to-apples’ year-over- year retention comparison.

2020 started slightly below 2019 levels, but the market showed early strength in February and March. As the US economy shut down due to the COVID-19 pandemic, we measured the highest single month drop in April of 6.9 points since launching the Index. As we entered summer, wholesale prices continued the rebound started during the second half of May, with a projected increase of about three points in June. Currently, the Index is still below last year’s value, as instead of spring price strengthening, we had a record drop due to the COVID-19 shut down.

During the last recession (2007-2009), the Index lost about 15 points in a span of 12 months before the recovery started. We project that during the current recession, the Index will decline in the next six months, but will start recovering afterwards in our most likely economic scenario. One of the main differences between this and the previous recession is the forced and abrupt shutdown of assembly lines and, as a result, significant reduction in projected used vehicle supply in 2021 and beyond.

Segment Highlight – Sporty Cars

Segment Overview

Sporty Cars, unlike the other Car segments, have experienced consistent market share over the years at roughly 2%. This is a niche segment that not all consumers can fit into their lifestyle, but for those that can, it is a segment that offers a fun to drive experience. The majority of the players in this segment only offer two door coupes and convertibles, but we have seen a few four door entries added to the segment, including the Volkswagen GTI and the recently released BMW 2-Series Gran Coupe. Three of the biggest players are domestics that fall into the “muscle car” category: Chevrolet Camaro, Dodge Challenger, and Ford Mustang. The rest of the segment is comprised of imports and range from the Mazda MX-5 Miata to the Audi TT.

Historical Trends

Long term Retention Index

Prior to the recession of 2008/2009, in general, the Black Book Retention Index for the Sporty Car segment remained positioned above the overall market Index, but like the market and most of the segments during that time, the segment level Index fell sharply, down to a low of 88.3 in May 2009. At times, the Index has been close to the market level Index, but it has yet to rise above that barometer. When shelter-in-place orders went into effect and values tumbled in April, the Index for the Sporty Car segment fell –6.6% to 99.3 as compared to the market Index that fell –6.9% to 106.0. The segment level Index continued to fall in May, but at a much lower pace, only down –0.5% to 98.9.

Recent depreciation rates

Historically, the Sporty Car segment is sensitive to seasonality, particularly due to the convertible trims, but this segment is also sensitive to region as only a few models in this segment offer AWD variants. During COVID-19, values trended along with the majority of the market in a downward trend, but during most weeks at a lower rate. This is likely due to the pandemic related shutdowns occurring in the springtime, which is typically a time that these vehicles experience some positivity in the marketplace. In recent weeks, this segment has experienced record setting increases, rivaled by the Compact Car segment for largest car segment increases for the last seven weeks. As for the more expensive Premium Sporty Car segment, the trend is similar, but at a lower level, experiencing increases solely over the last four weeks. The Premium Sporty Car segment also did not decline as much during the pandemic as some of the other segments.

Used Wholesale Price Projections

Wholesale Price Impact Under the Most-Likely Economic Scenario

Wholesale prices dropped significantly in April as uncertainty over COVID-19 impact and response dampened vehicle demand, resulting in an overall wholesale price decline of 5.9% in April. We saw a substantial improvement in prices during the last two weeks of May and the monthly decrease was limited to only -1.5% in May. As we entered June, wholesale prices continued to increase, and we now project that we will see an overall market appreciation for the entire month of June. As a comparison, last year’s prices declined by 0.9% over the same period.

Black Book’s preliminary July Published Residual Values (dashed lines) reflect a new economic reality. Together with the temporary strengthening in demand in June, projected values will continue to stay well below pre-COVID-19 projections over the next two years, with the deepest declines expected over the next six months. The green line represents our most-likely economic scenario that does not include a possible second wave of COVID-19, and a still undefined second stimulus package. A more severe and prolonged recessionary scenario is shown in red. Projections are indexed to the pre-COVID-19 projections (black line). All values are weighted by the used vehicle sales volume (actual, where available, or projected).

Short-Term Outlook (Summer / Fall of 2020)

We project a drop in wholesale prices compared to a pre-COVID-19 baseline this summer/fall, as the US economy suffers through the effects of COVID-19. We anticipate that later this summer and fall, the wholesale prices will be between 10% and 15% lower than originally projected before the pandemic, due to a glut in supply and much weaker demand. Prices will start to recover in 2021 as the economy becomes stronger. We also anticipate that older (>6-year-old), cheaper vehicles in average condition will not decline as much due to increased demand for these units.

Long-Term Projections (36-Month Residual Values, Summer / Fall of 2023)

The effects of the pandemic will continue to be felt, but we continue to project that values will return to the pre-COVID-19 baseline as used supply will decline as a result of cuts in retail and fleet sales throughout the remainder of 2020 and into 2021.

Wholesale Price Impact Under a Severe Recession Scenario

In this scenario, we project a drop in wholesale prices of more than 20% later in the summer and fall, compared to a pre-COVID-19 baseline, with a slow recovery in 2021. The effects of the pandemic and recession will still be impactful in 36 months, and we project a 10% market level decline of wholesale prices as compared to pre-COVID-19 projections for the second half of 2023.

Retail Vertical

Retail Prices

In the age of proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure the trends in the retail space. From the peak in early April until the end of May, retail listing prices decreased by about 5% – a much lower decline compared to wholesale prices. In the last ten days we saw a temporary stabilization of retail prices fueled by higher consumer demand due to stimulus payments and federal Paycheck Protection Program (PPP). We expect retail prices to continue their decline later in the summer as stimulus payments are exhausted and the protection in PPP expire.

Dealers Insights

Many dealers we’ve been in contact with reported a record-breaking May, but June hasn’t been as successful for them. However, they say this isn’t due to a lack of demand, but instead their lack of supply, new and used, prevented them from being able to complete the deals.

Lack of new inventory is one of the biggest pain points for dealers right now and they are turning to newer, low mileage, clean condition used units to fill in the gaps. This increased demand at the auctions for these hard to find units is continuing to push up prices on the lanes.

Production at most manufacturing facilities should be back to pre-COVID levels by next month, but this isn’t soon enough for dealers that are needing deliveries of new inventory. Dealers that are accustomed to receiving truckloads of new vehicles are only receiving 2-3 vehicles at a time right now.

As for what the dealers are saying is in demand right now, it’s full-size trucks, crossovers, and sporty cars.

Retail vs. Wholesale Trends

Each week, members of the Black Book automotive analyst team, data science team and executive leadership team speak with no less than 30 dealers, along with buyer and seller representatives, wholesalers and others, who represent hundreds of franchise and independent dealers nationwide. These industry experts, along with experts we speak with from leading fleet management and rental car companies, auction leadership, and other industry experts help to clarify and connect the dots between the wholesale and retail markets.

Since the start of the pandemic, we have been observing different trends in wholesale and retail prices. In April and May, wholesale prices declined at a higher rate compared to retail prices. As margins grew, dealers reported healthy profits on per vehicle basis. Retail prices displayed stickiness on the way down. Similarly, as wholesale prices came roaring back to pre-COVID-19 levels, retail prices are slow to recover, exhibiting the same stickiness on the way up. As wholesale to retail margins shrink, it is even more important for dealers to stay up to date on market movements. We are seeing this trend play out on dealership lots, where retail asking prices are not increasing at the same levels as wholesale transaction prices. This means dealers are paying more at auctions and through wholesale channels, but those increased wholesale acquisition prices, as a percentage, are not flowing through to the retail lots and online listings. The main driver of the slow increase in retail prices based on our conversations with dealers, is simply fear—fear of sitting on inventory for too long and the market making a quick reversal, which leaves them stuck with a vehicle they paid too much for. Dealer sentiment is quite clear—if they are going to pay up for a vehicle in this environment, they are choosing to turn them quickly, even with less margin than normal, to ensure they are not caught with high priced inventory when the market does shift.

The graph below shows this retail / wholesale dynamics since the start of the year. Prices are indexed to the first week. For example, if a vehicle at the beginning of the year with typical mileage had a value of $10,000 retail and $8,000 wholesale (a $2,000 margin), then the same vehicle would be $9,400 retail and $8,300 wholesale (a $1,100 margin).

New Vehicles Sales Outlook

Our New Sales Outlook remains unchanged from last week. We anticipate a significant reduction in US new vehicle sales in 2020 (both retail and fleet sales) due to continued reduction in consumer demand. This is a result of several ongoing factors, including less miles driven due to remote work and shelter-in-place initiatives, high unemployment, and an overall feeling of uncertainty by consumers. Overall, new sales were down 23% during the first five months of the year, compared to last year (with a 30% YOY decline in May as most states started to lift shelter-in-place orders). Even as OEMs are restarting assembly lines, there are significant challenges to get back to a normalized production schedule as we reported in previous updates. US manufacturers are planning to get back to pre-COVID-19 levels in July the earliest as new production protocols and supply chain disruption slowed down the re-opening.

In our base economic scenario, we project a 25% drop (compared to pre-COVID-19 projections) in new sales in 2020 to 12.7mm units. In a deep economic recession scenario, we project a 40% drop in new sales in 2020 to 10.2mm units.

In the longer-term, we expect new sales volume to return to pre-COVID-19 levels within five years.

Used Vehicle Supply Projections

Black Book projects a higher than expected used vehicle supply in the wholesale marketplace for the rest of 2020 due to several factors:

Delayed lease returns resulting from lease extensions offered by OEMs – more than 560,000 additional three-year-old units

Extensive de-fleeting by rental car companies, due to lack of consumer and business traveler demand and financial pressure to raise cash – at least 250,000 one- to two-year-old vehicles

Dramatic reduction in auction activities due to COVID-19 in March, April, and May

Increased repossessions due to deteriorating economic conditions in addition to delayed repossessions in April / May

Short Term Lease Return Projections

When we started the year, lease returns were projected to hit a record volume of above 4.1 million units. Once the pandemic was underway, and most manufacturing stopped, OEMs started to encourage lease extensions in order to push returns further into 2020 when they would be in a position to provide replacement vehicles. As a result, we project at least 560,000 additional units in the second part of 2020 (compared to the pre-COVID-19 estimates) due to a slowdown in sales in April / May, along with expected turn-ins of the lease extensions.

Rental Unit Returns

Business and leisure travel collapsed at the end of March. We expect a significant reduction in both categories for the remainder of 2020. In addition, there is no expectation that travel will return to pre-COVID-19 levels in the next several years. According to IATA (The International Air Transport Association), air travel will not return to pre-COVID-19 levels until after 2023. This puts tremendous financial pressure on rental companies that rely on air travel, to reduce both their current fleet and future acquisitions. At the end of May, Hertz filed for bankruptcy in North America as a result of the pandemic.

In addition to Hertz, we expect other rental companies to reduce their fleet during the summer and fall months to match lower demand for rentals. This practice will lead to over 250,000 additional rental units hitting the wholesale market over the next six months. Note that this is a base case scenario in which rental companies (excluding Hertz) can gradually reduce their fleet instead of a rapid-fire sale.

The graph below shows Black Book’s projections for rental returns. The purple line shows the difference between current (darker rectangles) and pre-COVID-19 projections (lighter rectangles).

In the longer term (later 2021 – 2023), the drop in rental return volume will benefit the price of newer used units, as supply will be limited.

Longer Term Used Returns Projections

With the reduction in retail and fleet sales over the next several years, we project approximately 75k used units per month less in the market in 2023, compared to previously projected returns. This lower level of used inventory will be beneficial to used car prices as supply will be limited, helping to bolster valuations.

Originally posted on F&I and Showroom

More Dealer Ops

Dealer Debrief: Defection Data & EV Updates

In this week's debrief, host Lauren Lawrence discusses how to use defection data to your advantage and the latest on EV sales and charging infrastructure.

Read More →

How Defection Data is Bridging the Dealership Conversion Gap

Lead volume is flat, cross-shopping is up and brand loyalty is in retreat. As confident sales teams keep losing buyers they thought they had, daily industry sales data is showing dealers exactly where their funnel is breaking and how to fix it without buying a single new lead.

Read More →

Dealer Debrief: Where are you losing customers?

In this week's debrief, host Lauren Lawrence discusses the hidden leaks in dealerships where you might be losing customers without even realizing it.

Read More →

Dealer Debrief: Improving Your Inventory Management

In this week's debrief, host Lauren Lawrence covers a new survey that shows what service technicians really want and two launches that could help improve your inventory and vehicle life cycle management.

Read More →

Ladies and Gentlemen, This Is a Dealership: Why the Fundamentals Still Decide Who Wins

A teaching moment by a legendary football coach happens to apply perfectly in the auto retail space. Learn what it is and how to use it to your store’s advantage.

Read More →

What Market Timing Mistakes Mean for Your Reinsurance Program

When volatility hits, dealer-owned reinsurance programs face a familiar temptation: pull back and wait for calmer waters. New data from BOK Financial shows why that instinct can quietly cost you years of surplus growth.

Read More →

Dealer Ads and the FTC

The agency has made it clear in recent enforcement actions and warnings, in auto retail and other industries, that advertised prices must include all nonoptional costs to the consumer.

Read More →

Used Autos Supply Dwindles

The March shopping surge, despite high prices, cut into inventory by the most since the thick of the pandemic, Cox Automotive analysts calculated.

Read More →

Managing Risk Effectively Through Changing Times

The variables influencing risk pricing have changed significantly over the past five years. Being proactive and responsive to emerging trends is not optional but essential.

Read More →

Survey Reveals What Won't Fix What's Breaking Car Sales

AutoPayPlus says extra-long auto loans are trapping consumers and threatening the dealer trade-in cycle, and that the industry is leveraging the wrong tools to combat high MSRPs.

Read More →