BLACK BOOK – Specialty Market Insights

Motorcycle & Powersports Market Update

“Much like the last few months, Powersports values for March have mostly reverted to pre-pandemic adjustment patterns. As we head into the Spring market, prices across the majority of segments have risen this month. The increases are smaller than we would have seen in years past, but average unit prices are still a good 20 percent or more higher than historical averages. The inventory crunch of the past two years also appears to be lessening in concert with our return to more normal market rhythms.”– Scott Yarbrough, Senior Analyst, Motorcycle & Powersports

February to March Average Segment Change in Value

Scooters are our biggest movers this month, up 1.9%. This is a highly seasonal segment that typically sees large increases in value as we head towards warmer weather. The ATVs are the only other segment to change in value by more than a percent, up 1.3%. Nearly all other segments have seen minor increases of roughly half a percent, and a few have declined by negligible amounts. The key takeaway from the above numbers is not that these increases are smaller than we would have seen in years past, but that overall pricing levels are still running 20 percent or more above normal. Even with these small increases in value, average prices are still at historically high levels, and will likely remain that way for the rest of the year. We expect the current trend of smaller than normal adjustments to continue through the summer.

Segment Spotlights & Industry News

Cruiser Performance

After decreases in value, however minor, over the past few months, the Cruisers are now seeing a fairly typical spring boost in values. The amount of the increases are smaller than historical averages would suggest, but overall pricing levels are still running nearly 40% (yes you read that correctly) higher than 2019 values. Until the supply of inventory, both new and used, more completely catches up with demand, we expect these extraordinary pricing levels to remain with us.

ATV & Utility Vehicle Segment Performance

The ATVs and Utility Vehicles are, much like most other segments, behaving as they did in the past. Compared to last year where nearly every month they increased in value, they actually declined a bit this winter, and are now headed back up. Utility Vehicle pricing is up over 40% from 2019, and ATVs are actually up a bit more than the side-by-sides during the same time period. The off-road segments continue to be some of the biggest economic winners from the pandemic.

Harley-Davidson reported Q4 2021 results showing revenues rose 54% YoY to $816 million. This was due to increased wholesale shipments, a profitable product mix, and increased pricing. Motorcycle revenue increased 71% YoY to $546 million. Sales were up 39% to 29,100 units.

US job growth once again greatly exceeded estimates in the latest numbers released by the Labor Department. Unemployment is currently 3.8% as the economy added 678,000 nonfarm jobs in February. The gains were widespread, led by gains in leisure and hospitality, professional and business services, health care, and construction according to the government.

The biggest current threat to another good year for the Powersports industry is the recent Russian invasion of Ukraine and its aftermath. Gas prices are already at historical highs, having risen 74 cents in just one week. As companies pull out of the Russian market, and supply chains are further disrupted across the globe, there will be new challenges to be navigated for everyone.

Collectible Cars Market Update

“The various auctions held at Amelia Island last week generally did very well, with total sales coming in at over $125 million. Almost all of the cars at this venue are naturally in very good condition, but the vehicles that seemed to do the best against their pre-sale estimates were the ones in ‘beyond excellent’ condition, the truly stunning examples. Sell throughs were high across the board, indicating continued strong interest from buyers.”– Eric Lawrence, Principal Analyst, Specialty Markets

Auction Activity

RM Sotheby’s 23rd annual Amelia Island auction, held at the Ritz-Carlton, was the official auction of the Amelia Island Concours d’Elegance. It was very successful, with total sales of $46,636,640 and an impressive 89% sell through percentage. The vehicles offered for sale covered almost the entire collectible vehicle spectrum, with two of the top five sellers being from the 1930s and the other three being less than ten years old. The rest of the top ten was rounded out with the usual assortment of vehicles from the years in between.

Bonhams’ Amelia Island auction, held at the Fernandina Beach Golf Club, was very successful, with a 95% sell through ratio and total sales of $15 million. The highlight of their sale was a 1955 Porsche 550 Spyder. This particular example had an extensive in-period racing history, had not been offered for sale in more than fifty years, and ended up selling for $4,185,000 after a spirited battle between bidders. Another seven-figure result was achieved by a beautiful 1929 Duesenberg Model J Convertible Victoria, which brought $1,066,500.

Gooding & Company’s Amelia Island auction, held at the Omni Amelia Island Resort, was the most successful event in their thirteen-year history there. Total sales came in at $66,534,480 with a sales rate of 92% (91/99). An incredible nineteen lots sold for more than $1,000,000, with the average amount being $731,148. Additionally, seven of the vehicles sold for new world records. The undisputed star of the auction was the 1937 Talbot-Lago T150-C-CS Teardrop Coupe, which sold for $13,425,000, the most ever for a French automobile sold at auction. Another huge result was the 1967 Toyota 2000 GT Coupe, which sold for $2,452,500, making it the most expensive Japanese car ever sold at auction.

Notable Recent Auction Sales Include:

1937 Talbot-Lago Teardrop Coupe Courtesy of Gooding

2015 Ferrari LaFerrari $3,662,500 (RM Sotheby’s)

2019 Bugatti Chiron Sport $3,360,000 (RM Sotheby’s)

2020 McLaren Speedtail $2,700,000 (RM Sotheby’s)

1955 Mercedes-Benz 300SL Gullwing $2,040,000 (RM Sotheby’s)

1971 Mercedes-Benz 280SE 3.5 Cabriolet $324,000 (Bonhams)

1957 Porsche 356A 1600 Speedster $302,000 (Bonhams)

1968 Lamborghini 400GT 2+2 Coupe $318,500 (Bonhams)

1954 Bentley R-Type Continental Fastback $2,975,000 (Gooding)

1991 Ferrari F40 $2,452,500 (Gooding)

1959 BMW 507 Series II $2,150,000 (Gooding)

Market Trends

The Vintage Pickup Truck segment was originally limited to domestic full-size pickups, but has recently expanded to include collectible SUVs, many of which were constructed on a modified truck chassis. A few examples within this segment are the Ford, Chevrolet/GMC, and Dodge pickups built from the mid-1940s up through the early 1970s, Jeep CJs, Toyota Land Cruiser FJ40s, International Scouts, early Range Rovers, and first-generation Chevrolet Blazers and Ford Broncos. Pickups have been on a run for the better part of a decade, and SUVs have been on fire for the past two or three years, with values doubling or sometimes tripling during that time frame. During the past year, many Vintage Pickups and SUVs have increased anywhere from 20 – 25%.

All of the various collectible vehicle segments we track increased in value last month, including Vintage Muscle Cars, Vintage Pony Cars, American Classics, Vintage European Sports Cars, Vintage Exotics, and Classic Trucks and SUVs. This is the first time in quite a while that all of the segments have increased month over month. Several of the “big” auctions of the year have recently wrapped up (Scottsdale, Amelia Island, Kissimmee, etc.) and the results from almost all of them have been spectacular. Several world records have been set, and the sell through ratios have all been strong. There are several more auctions on the horizon, and we’ll be watching them closely.

Recreational Vehicles Market Update

“With the approach of Spring and warmer weather in many parts of the country, we are beginning to see some changes in the RV market. Towable values increased moderately, reversing three consecutive months of declines, and although Motorized units did not also increase, their drop off was only a fraction of a percent, a marked improvement over last month’s sharp decline.”Eric Lawrence, Principal Analyst, Specialty Markets

Wholesale RV Values Mixed As Spring Approaches

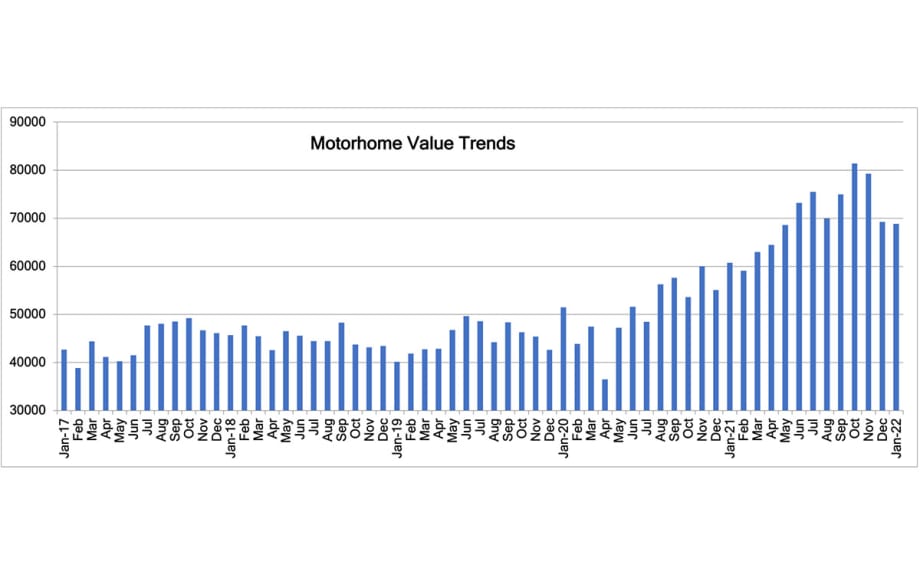

For Motorhomes (including Class A, B, and C):

Average selling price was $68,842, down $395 (0.5%) from the previous month.

One year ago, the average selling price was $60,739.

Auction volume was up 2.5% from the previous month.

The average model year was 2011.

For Towables (including Travel Trailers and Fifth Wheels):

Average selling price was $21,865, up $1,345 (6.5%) from the previous month.

One year ago, the average selling price was $19,570.

Auction volume was up 6.8% from the previous month.

The average model year was 2016.

Industry Highlights

According to the RVIA, the total number of RVs shipped in January was 53.290, an increase of 16.0% over January 2021. Towables totaled 48,565 units and Motorhomes accounted for 4,725. Truck Campers came in at 395, Folding Camping Trailers reached 679, and Park Models were 332. Class B motorhomes (Van Campers) ended the month with 1,303 shipped, Class A’s totaled 1,269, and Class C’s finished with 2,153.

The RVIA announced that they are predicting RV sales of 591,100 for 2022, with an expected range from 578,000 – 603,300. This would be down slightly (-1.5%) from 2021’s total of 600,240.

Statistical Surveys, Inc. reported that there were 567,079 RV registrations in North America in 2021, a new record, up 8.4% from 2020. The segments that did the best were Class B Motorhomes (+36%), Fifth Wheels (+22%), Truck Campers (+11%), and Travel Trailers (+7%).

The Baird RV Dealer Survey found that responding dealers were positive on both current market conditions (64 of 100) and the three-to-five-year outlook (59 of 100). A score over 50 is considered positive.

Camping World reported 2021 revenue of $6.9 billion, an increase of $1.5 billion (26.9%) over 2020.

Commercial Truck Market Update

“Medium and Heavy-Duty Truck values remain strong as demand continues to increase. We are seeing strength and stability in Wholesale, Retail, and Auction transactions all across the country. There are simply not enough trucks in the market to keep up with the increasing freight, construction, and last mile delivery demand. Everywhere we turn, supply chain issues are causing prices for goods and services to increase. Fuel prices have been increasing over the past 14 months and are expected to continue to rise as the conflict between Russia and Ukraine continues. This conflict will likely cause further delays in new truck production; helping to further strengthen new and used Commercial Truck values. “ – Josh Giles, Principal Automotive Analyst

Medium-Duty Trucks

The chart above illustrates monthly adjustment amounts for Medium-Duty cab/chassis units in classes 3 through 6 for model years 2011-2018.

Heading into March, Medium-Duty truck values increased an overall weighted average of $54 (0.1%) compared to the $150 (0.4%) increase seen the month prior.

Over the past twelve months Medium-Duty units (2011-2018) have increased $10,347 (33.7%), from an overall weighted average of $24,645 to $39,919.

Over the past ten years Medium-Duty truck values (4-10 year old) have increased 117%, from an average of $18,104 to an average of $39,919.

Due to increasing demand and supply chain issues, prices are well above what is typical for this market. We do not anticipate new truck production to increase enough this year to have a major impact on used pricing. We expect values to continue to slowly increase over the next couple of months before leveling off and stabilizing for the remainder of the year.

Heavy-Duty Trucks and Tractors

The chart above illustrates the average monthly adjustment amount for Heavy-Duty Trucks and Road Tractors within classes 7 and 8 (2011-2018).

From February to March, Construction/Vocational Units increased an overall weighted average of $605 (0.7%) compared to the 1,269 (1.6%) increase seen the month prior.

Over-the-Road units increased an average of $214 (0.4%) heading into March, compared to the $160 (0.3%) average increase seen the month prior.

Regional Tractors followed a similar trend, increasing an average of $227 (0.4%) from February to March, compared to $133 (0.3%) average increase seen the month prior.

Over the past twelve months, Construction/Vocational (2011-2018) average values have increased $19,691 (28.1%), Over-the-Road Tractors have increased $17,987 (44.0%), and Regional Tractor values increased $17,962 (50.9%).

Over the past ten years, 4–10 year old Construction/Vocational models have increased an average of $27,303 (48.8%), Over-the-Road Tractors have increased an average of 25,371 (79.9%), and Regional Tractors have increased an average of $24,579 (92.9%).

Commercial Trailer Market Update

Commercial Trailer values continue to increase as freight demand increases and New and Used Commercial Trailer inventory shrinks.

Wholesale and retail transactions on all trailer segments continue a positive trend as demand continues to rise.

In addition to transportation, some trailers are used as storage. With freight being backed up due to supply chain issues and driver shortages, Dry Vans, Refrigerated Vans, and Lowbed trailer demand has surpassed the rest of the segment.

Dry Van values have increased 8.4% during the fourth quarter of 2021. Dry Vans increased 17.8% during Q3 of 2021.

Dump Trailers increased just 2.0% heading into 2022. This segment was flat during Q2 of 2021. We expect demand and values for this segment to increase over the next 6-8 months as operators are having to resort to using more Dump Trailers because new Dump Truck production issues continue to grow.

Refrigerated Van values increased 9.0% heading into January. This segment increased 14% from Q4 of last year.

Much like the truck segments, we do not expect trailer values in 2022 to increase at the rate we experienced in 2021. We expect trailer values a year from now to be around the same value they are today.

Retail and Freight Demand

According to Federal Reserve Economic Data (FRED), new retail sales for Commercial units in classes 4 through 8 were reported at 33,656 units in February of 2022. This is down 2,866 units from January.

We expect to see these retail sales figures stabilize and slowly begin to increase towards the fourth quarter of 2022.

ATA Truck Tonnage is one of the many leading indicators when it comes to the strength and stability of the trucking and freight industry. For the 6th consecutive month, we’ve seen this number rise, which is wonderful news as distribution companies work to release some of the congested ports.

In December of 2021, ATA Truck Tonnage was reported at 114.8% compared to November’s rate of 113.7%.

Freight demand remains strong and continues to trend in a positive direction. However, as the conflict between Russia and Ukraine escalates, we may see ATA Truck Tonnage drop as this conflict will impact importing and exporting from that region.