Black Book: Specialty Market Update

For the second month in a row, the average wholesale auction prices of all the major RV market segments declined.

For the second month in a row, the average wholesale auction prices of all the major RV market segments declined.

BLACK BOOK – Market Insights: 2/9/2022

Motorcycle & Powersports Market Update

“Our second month of the new year again shows a Powersports market working its way back towards traditional seasonal valuation patterns, but not quite there yet. Most segments are showing a decline in values like years past, but the amounts are generally smaller than would be expected for the time of year. Additionally, the Street bikes are up, a very unusual occurrence pre-pandemic. Also, with the economy heating up, we expect the recent softening in prices we have seen lately to slow down a bit.”– Scott Yarbrough, Senior Analyst, Motorcycle & Powersports

January to February Average Segment Change in Value

With the exception of the Personal Watercraft and Jet Boat segments, only the Off-Road bikes have dropped in value by over 1.0% this month. For the middle of winter, to have all the other segments drop only about half a percent on average shows that we are: a) finally beginning to see traditional seasonal valuation patterns from the pre-pandemic era again, and b) still have a ways to go before the market actually behaves like it did before. The Street Bikes are especially noteworthy as they are up by 1.1%, and this coupled with the other on-road segments dropping a mere .5% on average, shows how continued strong demand in the market coupled with ongoing supply shortages are keeping prices elevated. We expect a gradual return to more normal pricing patterns as the year progresses, but progress will be slow and uneven.

Segment Spotlights & Industry News

Cruiser Performance

The Cruiser segment has cooled off quite a bit compared to its performance a year ago, but what has not changed is the overall pattern in value changes. A year ago, this segment was slowly but surely increasing in value each month from October onwards, whereas this year it is decreasing slightly month over month during the same period.

Off-Road Segment Performance

The Off-Road Bikes tell a very different story from the Cruisers segment. Last year they were still on a remarkable run that saw them increase in value nearly every single month from spring of 2020 through last year. These bikes are currently still in high demand, but seeing a lot of volatility from month to month as the market searches for an equilibrium point.

Snowmobiles are seeing increased demand this winter and suffering from the same supply chain issues as other Automotive and Powersports vehicles. New inventory is sold out at many dealers and incoming production from the OEMs is failing to keep showrooms stocked.

Continuing supply chain issues and production delays are also impacting retailers on the Personal Watercraft side of the industry, several dealers we have spoken with report selling out nearly all of their 2022 new units and reduced allocations from the OEMs. This is forcing many to turn to the used market to keep inventory levels up. We expect another good year for water based powersports vehicle values.

US job growth greatly exceeded estimates in the latest numbers released by the Labor Department. Unemployment is currently at 4.0% and nonfarm jobs increased by 467,000 in January. Revised numbers for November and December showed an increase of 709,000 jobs for those months. Average hourly earnings are up 5.7% year over year. A strong economy should set the stage for another good year in Powersports.

Collectible Cars Market Update

“The January collectible car auctions wrapped up a week or so ago, and the results were very impressive. Total sales for the month came in at nearly $480 million, with Mecum’s Kissimmee auction accounting for $213 million and the various Scottsdale auctions contributing $267 million. Sell through rates were some of the best we have seen in a while, with Mecum reaching 90% and Scottsdale topping 95%.”– Eric Lawrence, Principal Analyst, Specialty Markets

Auction Activity

RM Sotheby’s 23rd annual Scottsdale auction, held at the world-famous Arizona Biltmore hotel, saw sales totals reach $43.3 million, with 95% of all lots being hammered sold. Bidders hailed from thirty different countries, with 24% being first time bidders.

Mecum’s Kissimmee, Florida auction, held over the course of eleven days at Osceola Heritage Park, set a new collectible car auction record for a single event with sales of $217 million and a sell-through rate of 90%. They also set a company record for the highest single day total, with $72 million. Thirteen vehicles sold in excess of $1,000,000.

Gooding & Company’s hybrid Scottsdale auction allowed attendees to view vehicles in person, but then place bids on them through their Geared Online remote bidding platform. Sales were brisk, totaling nearly $7 million with an 88% sell through.

Bonhams’ eleventh annual Scottsdale auction, held at the Westin Kierland Resort, achieved sales of roughly $12 million with a sell through percentage of 96%.

Barrett – Jackson’s Scottsdale auction was the most successful event in the company’s 50 year history. Total sales came in at $203 million, and all 1,857 vehicles that crossed the block were sold at No Reserve.

Worldwide’s Scottsdale auction achieved sales totals of nearly $10 million with a sell through ratio of 92%.

Notable Recent Auction Sales Include:

2004 Porsche Carrera GT Coupe $1,980,000 (Barrett – Jackson)

2014 McLaren P1 Coupe $1,705,000 (Barrett – Jackson)

1955 Mercedes-Benz 300SL Gullwing Alloy Coupe $6,825,000 (RM Sotheby’s)

1987 Porsche 959 Komfort Coupe $1,600,000 (RM Sotheby’s)

1958 AC Ace Roadster $516,500 (Bonhams)

1949 Buick Roadmaster “Rain Man” Convertible $335,000 (Bonhams)

1929 Duesenberg Model J Derham Sedan $2,260,000 (Worldwide)

1991 Lamborghini Diablo Coupe $302,000 (Worldwide)

1961 Maserati 500GT Touring Coupe $924,000 (Gooding)

1974 Ferrari Dino 246 GTS Spider $374,000 (Gooding)

1968 Chevrolet Corvette 427/390hp Courtesy of Bonhams

Market Trends

The Vintage Pony Car segment represents mid-sized sporty vehicles from American Motors, Ford, General Motors, Dodge, and Plymouth produced from the mid-1960s through the early 1970s. A few representative examples would include its namesake Ford Mustang, Chevrolet Camaro, Mercury Cougar, Pontiac Firebird, Plymouth Barracuda, Dodge Challenger, and AMC Javelin. These vehicles dipped in late 2017 but have been on the rebound ever since. They are typically less expensive than those in the Muscle Car segment, and their generally high production numbers (over 1,000,000 Mustangs in 1965-66 alone) make them a popular choice for collectors, especially those new to the hobby. Parts availability is generally pretty good, especially for Ford and GM products, and many of these cars represent their owner’s first attempt at a restoration.

The majority of the collectible vehicle segments we track increased in value last year, including Muscle Cars, Pony Cars, American Classics, Vintage Exotics, and Classic Trucks & SUVs. Only Sports Cars declined, and it was not a huge amount. As we have said before, many of these cars, especially early Porsches, had skyrocketed in value a few years ago, so it is completely normal and expected that they will need a little time to find their equilibrium. The various collectible car auctions in Arizona last month were very well attended by serious bidders, and there were many strong sales, especially for vehicles in excellent (or even beyond excellent) condition. Although it’s hard to make a blanket statement about the overall health or direction of the market based on a relatively small number of sales (and most of those sales being for “the best of the best” examples), I will say that the recent Scottsdale auctions certainly pointed in the right direction that the collectible market will continue to stay strong during the upcoming year.

Recreational Vehicles Market Update

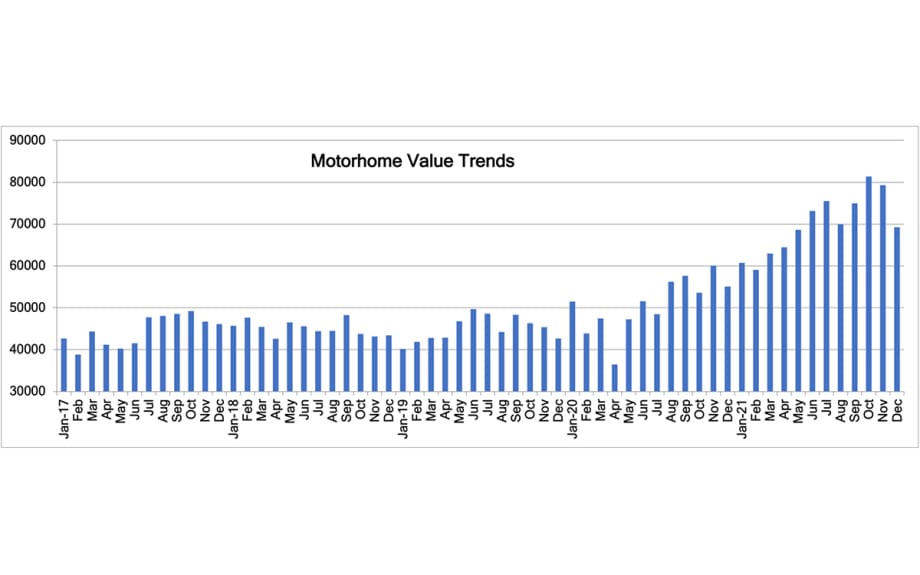

“For the second month in a row, the average wholesale auction prices of all the major RV market segments declined. This is not surprising given the time of year, as specialty vehicles often see lower demand during the colder months. Motorhomes dropped more than towables, but it’s noteworthy that their average age was two years older than last month (MY2009 vs MY2011).”Eric Lawrence, Principal Analyst, Specialty Markets

Wholesale RV Values Decline For Second Month In A Row

For Motorhomes (including Class A, B, and C):

Average selling price was $69,237, down $10,033 (12.6%) from the previous month.

One year ago, the average selling price was $55,072.

Auction volume was down 14.9% from the previous month.

The average model year was 2009.

For Towables (including Travel Trailers and Fifth Wheels):

Average selling price was $20,520, down $885 (4.1%) from the previous month.

One year ago, the average selling price was $18,191.

Auction volume was down 12.8% from the previous month.

The average model year was 2016.

Industry Highlights

According to the RVIA, the total number of RVs shipped in December was 40,347, a slight decrease of 0.1% under December 2020. Towables totaled 36,908 units and motorhomes accounted for 3,439. Truck Campers came in at 493, Folding Camping Trailers reached 652, and Park Models were 244. Class B motorhomes (Van Campers) ended the month with 912 shipped, Class As totaled 901, and Class Cs finished with 1,626.

The RVIA announced that the final RV shipment total for 2021 came in at 600,240, which was a new yearly record. It broke the previous record of 504,599, which had been set in 2017, by 19%.

Lazydays RV reported fourth quarter 2021 revenue of $323 million, with net income of $15.3 million, both increases over 2020.

RV Retailer opened a new location in Jacksonville, Florida, their eighth in the state and 94th overall.

European RV sales rose nearly 10% year over year, with sales approaching 260,000 units.

The 2022 Florida RV Supershow was very well attended and featured several e-RV concept introductions.

Kampgrounds of America (KOA) announced that their revenue increased 33.2% over 2020, setting an all-time record.

Medium and Heavy-Duty Truck & Commercial Trailer Market Update

“Harsh weather across the country is helping to increase demand on construction and last mile delivery units. This past month we watched both wholesale and retail prices continue to climb for Construction and Medium-Duty trucks as new and used trucks become even more scarce. Regional and Over the Road Tractor prices dropped just a bit overall this past month due to some lagging inventory in the sales channels. Recent conversations with OEMs, remarketers, and dealers across the country lead us to believe that there is an opportunity for values to remain stable and increase in some areas depending on availability. The wholesale market will likely remain in a holding pattern for the next 8 – 10 months as there are simply not enough trucks in the market to keep up with freight and construction demand.”– Josh Giles, Principal Automotive Analyst

Medium-Duty Trucks

Above we see both the monthly adjustment amounts and the overall weighted average value trends for Medium-Duty cab/chassis units in classes 3 through 6 for model years 2011-2018.

From January to February, Medium-Duty trucks increased an overall weighted average of $150 (0.4%) compared to the $1,840 (4.9%) increase seen from December to January

Over the past twelve months Medium-Duty units (2011-2018) have increased $10,124 (32.9%), from an average of $24,103 to $39,865.

Due to supply chain issues, prices in this market are already extremely high compared to where they should be. We do not anticipate new truck production to increase enough this year to have a severe impact on used pricing. We expect values to continue to slowly increase over the next couple of months before leveling off and stabilizing for the remainder of the year.

Heavy-Duty Trucks and Tractors

Above we see both the monthly adjustment and the overall weighted average value trends for Heavy-Duty trucks and road tractors in classes 7 and 8 for model years 2011-2018.

From January to February, Construction trucks increased an overall weighted average of $1,269 (1.6%) compared to the $4,652 (6.1%) increase seen the month prior.

Over-the-Road units increased an average of $160 (0.3%) from January to February, compared to the $1,829 (3.3%) average increase seen the month prior.

Regional Tractors increased an average of $133 from January to February, compared to $1,672 (3.4%) average increase seen the month prior.

Over the past twelve months Construction/Vocational (2011-2018) average values have increased $18,342 (26.1%), Over-the-Road Tractors increased $17,706 (43.4%), and Regional Tractor values increased $17,320 (48.9%).

We believe there is an opportunity for values in some segments to continue increasing before beginning a stabilization trend.

Commercial Trailer Market Update

Commercial Trailer values continue to increase as new production issues are causing scarcity in both new and used inventory.

Wholesale and retail transactions on all trailer segments continue a positive trend as demand continues to rise.

In addition to transportation, some trailers are used as storage. With freight being backed up due to supply chain issues and driver shortages, Dry Vans, Refrigerated Vans, and Lowbed trailer demand has surpassed the rest of the segment.

Dry Van values have increased 8.4% during the fourth quarter of 2021. Dry Vans increased 17.8% during Q3 of 2021.

Dump Trailers increased just 2.0% heading into 2022. This segment was flat during Q2 of 2021. We expect demand and values for this segment to increase over the next 6-8 months as operators are having to resort to using more Dump Trailers because new Dump Truck production issues continue to grow.

Refrigerated Vans values increased 9.0% heading into January. This segment increased 14% from Q4 of last year.

Much like the truck segments, we do not expect trailer values in 2022 to increase at the rate we experienced in 2021. We expect trailer values a year from now to be around the same value they are today.

Retail and Freight Demand

According to Federal Reserve Economic Data (FRED), new retail sales for commercial vehicles in classes 4 through 8 were reported at 36,315 units. This is down 10,427 units from December when retail sales were reported to be 47,042.

We expect to see these retail sales figures stabilize and slowly begin to increase towards the fourth quarter of this year.

ATA Truck Tonnage is one of the many leading indicators when it comes to the strength and stability of the trucking and freight industry. For the 5th consecutive month, we’ve seen this number rise, which is wonderful news as distribution companies work to release some of the congested ports.

In November of 2021 ATA Truck Tonnage came in at 114.4% compared to October’s rate of 113.5%.

Freight demand remains strong and continues to trend in a positive direction. Hopefully, supply chain issues will improve, leading to more trucks and trailers entering the market as distribution numbers in North America are expected to continue increasing

More Fixed Ops

Extreme Temps Hinder EV Efficiency

American consumers might be happy to know that their preferred hybrids are slightly less impacted by extreme temperatures than fully electric vehicles, according to a new study.

Read More →

Ban on Air Bag Inflators by Chinese Maker Proposed

NHTSA blames 10 deaths and two serious injuries on what its investigators believe were illegally imported air bag inflators. It’s taking public comments before deciding whether to ban them outright.

Read More →

Fix It Forward Program Helps Man Regain Mobility

Albuquerque consumer who suffered a life-changing injury regains the use of his vehicle after Fiesta Volkswagen's service team shared his story with DOWC Cares.

Read More →

ASE Connects Partners With Worldpac to Build Technician Numbers

The collaboration is intended to help auto dealerships, automakers and after-market shops further develop the technician pipeline.

Read More →

Not as Tickled With Tires

U.S. consumers are finding less satisfaction with the rubber that meets their roads, though their loyalty to tire brands has lately inched up.

Read More →

Auto Recalls Sank Last Year

2025 Sedgwick data indicate that the number of vehicles affected fell to its lowest point in more than a decade.

Read More →

ASE Winter Registration Now Open

The deadline to register for the industry standard certification testing is March 31.

Read More →

U.S. Drivers Overdue for Major Services

Data shows dealers have ample opportunity ahead of the holiday travel season.

Read More →

Auto Dealers Losing Service Customers

Study finds that though overall service drive revenue is up, loyalty is eroding

Read More →

Jeeps Can Catch Fire

Hundreds of thousands recalled, some for second time, to address battery flaw

Read More →