Black Book: Weekly Market Report

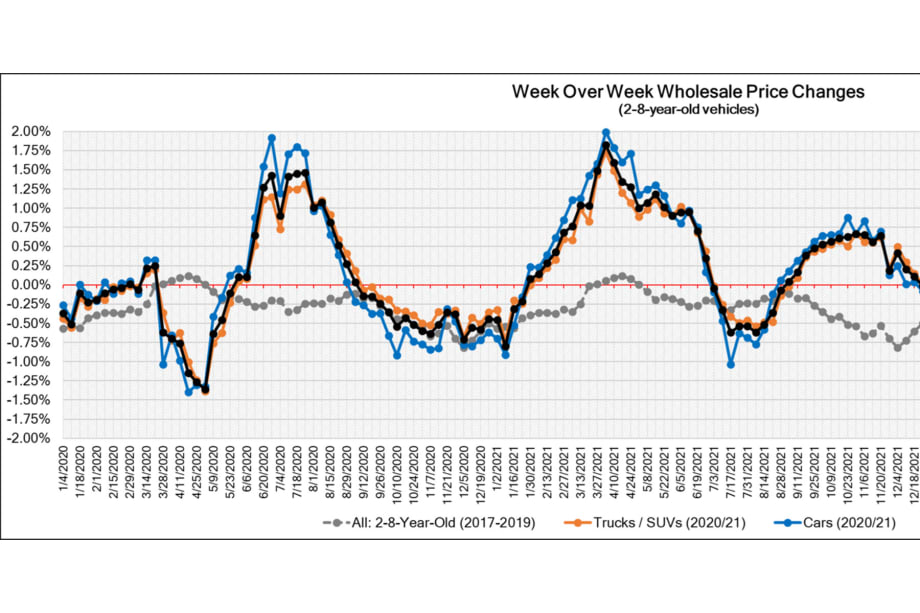

Repossessions are beginning to show up in the market and with fuel prices returning to a level last seen in February of this year, the Car segment valuations are taking the hardest hit.

Repossessions are beginning to show up in the market and with fuel prices returning to a level last seen in February of this year, the Car segment valuations are taking the hardest hit.

Black Book Market Insights

Wholesale Prices, Week Ending October 15th

Remarketing strategies are varying from seller to seller and last week, we saw some sellers adjusting floors and off-loading inventory, while others held firm to floors. Repossessions are beginning to show up in the market and with fuel prices returning to a level last seen in February of this year, the Car segment valuations are taking the hardest hit.

This Week Last Week 2017-2019 Average (Same Week)

Car segments -1.11% -0.66% -0.45%

Truck & SUV segments -0.67% -0.75% -0.39%

Market -0.82% -0.72% -0.41%

Car Segments

On a volume-weighted basis, the overall Car segment decreased -1.11%. For reference, the previous week, cars decreased by -0.66%.

All nine Car segments decreased last week.

Four segments reported declines greater than 1% last week: Compact Car (-1.41%), Near Luxury Car (-1.34%), Prestige Luxury Car (-1.34%), and Sporty Car (-1.31%).

Premium Sporty Car reported the smallest decline at -0.33%.

Sub-Compact Car (-0.75%) had the largest single week decline for the segment since August 2021.

Truck / SUV Segments

The volume-weighted, overall Truck segment decreased -0.67%, which is consistent with the prior week’s decrease of -0.75%.

All thirteen truck segments reported declines.

Small Pickups (-0.98%) reported the largest Truck segment decline last week, and Compact Crossovers were not far behind, with a decline of -0.94%.

Full-Size Vans (-0.05%) continued to decline, but the rate of decline is minimal with the past five weeks averaging -0.09% depreciation each week.

Weekly Wholesale Index

Calendar year 2020 and 2021 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g., 2019 calendar year) in the wholesale market were not observed for most of the last 2 years. We saw a similar picture in 2009, at the end of the Great Recession. Calendar year 2021 did not have typical seasonality patterns as the market had rapid increases in wholesale values for the majority of the year. The Wholesale Weekly Price Index reached the highest point of the year at the end of December 2021, reporting over 1.51 points.

The graph below looks at trends in wholesale prices of 2-6-year-old vehicles, indexed to the first week of the year. The index is computed keeping the average age of the mix constant to identify market movements.

Retail (Used and New) Insights

Hyundai Glovis, a subsidiary of the Hyundai Kia Automotive group, has acquired Greater Erie Auto Auction, a family-owned automotive auction in Pennsylvania, to expand into the US wholesale market. They plan to have auction sites in 6 cities by the end of 2025.

Mercedes-Benz unveiled the new EQE SUV, which is expected to have more than 300 miles of range per charge. An AMG variant will be available beginning for model year 2024.

Polestar has revealed the Polestar 3, an all-electric mid-size crossover; this first crossover from the Swedish electric vehicle startup is expected to arrive in the US late next year and start around $85,000.

The Sony-Honda joint venture focused on electric vehicles, Sony Honda Mobility, recently teased a concept car that is expected to be unveiled at the January CES conference. Customers can start placing orders for the new car in 2025 with deliveries expected in 2026.

Lucid’s over-the-air software, now called Lucid UX 2.0, has started its initial rollout phase and is expected to add an instant-on feature, enhanced driver assists, reconfigured controls, and more.

Used Retail Prices

Used Retail Prices are more accessible than in years past, due to the proliferation of ‘no-haggle pricing’ for used-vehicle retailing. Transparent pricing upfront makes the car buying process more enjoyable for customers and allows Black Book to accurately measure retail market trends.At the on-set of the pandemic, in CY2020, used retail prices increased slightly, following typical seasonal patterns, and then began dropping in April, finally hitting a low point in the late spring months. By late summer of CY2020, Used Retail Prices increased as supply of new vehicle inventory started to become scarce, but retail demand slowed down at the end of CY2020, resulting in declining retail asking prices for the last several weeks of the year. When CY2021 kicked off, demand rebounded while retail prices lagged slightly behind wholesale prices; March of 2021 started the dramatic increases in Used Retail Prices, fueled by stimulus payments, tax season, and shortages of new inventory. During the third quarter, retail prices continued to rise at a slower rate but soon picked up the pace once again to start the fourth quarter. In Q4, prices on retail listings steadily increased week after week. As CY2021 came to an end, the retail listing price index closed 36% above where the year began.Now in the fourth quarter of 2022, the Retail Listings Price Index has started to decline, but not as steep as the wholesale price index.

This analysis is based on approximately two million vehicles listed for sale on U.S. dealer lots. The graph below looks at 2-6-year-old vehicles. The Index is computed keeping the average age of the mix constant to identify market movements.

Inventory

Used Retail

Used retail active listing volume remained around 1.13 (meaning that the volume is about 13% higher than at the beginning of this year).

The Used Retail Days-to-Turn Estimate is around 43 days.

Wholesale

Floors are still high, but buyer count is stable. The inventory is there and has been consistent over the last few weeks. Some sellers seem to be adjusting their floors and are off-loading inventory, while others continue to hold firm to floors. Many buyers continue to hold out for lower prices or better condition vehicles, but others were actively online competing. Large independent dealers and rental companies were very active challenging each other to the best bid. Franchise dealers were still bidding, but the large independent dealers and rental companies seemed to dominate over them. Overall, sales rates were down this week, but certain lanes had higher sales rates than we have recently seen. This could potentially mean that sellers will soften their floors and sales rates could potentially get better. We still have not seen flood vehicles from the hurricane coming through yet, but there is speculation that a lot of cars were damaged, and they will be coming through the lanes soon. Moving into the fourth quarter, we anticipate an increase in repossessions being offered in auction lanes and we are starting to see more coming through. Overall, it was another stable week with the market still decreasing.

The Estimated Average Weekly Sales Rate dropped to 54% last week.

Originally posted on F&I and Showroom

More Fixed Ops

Extreme Temps Hinder EV Efficiency

American consumers might be happy to know that their preferred hybrids are slightly less impacted by extreme temperatures than fully electric vehicles, according to a new study.

Read More →

Ban on Air Bag Inflators by Chinese Maker Proposed

NHTSA blames 10 deaths and two serious injuries on what its investigators believe were illegally imported air bag inflators. It’s taking public comments before deciding whether to ban them outright.

Read More →

Fix It Forward Program Helps Man Regain Mobility

Albuquerque consumer who suffered a life-changing injury regains the use of his vehicle after Fiesta Volkswagen's service team shared his story with DOWC Cares.

Read More →

ASE Connects Partners With Worldpac to Build Technician Numbers

The collaboration is intended to help auto dealerships, automakers and after-market shops further develop the technician pipeline.

Read More →

Not as Tickled With Tires

U.S. consumers are finding less satisfaction with the rubber that meets their roads, though their loyalty to tire brands has lately inched up.

Read More →

Auto Recalls Sank Last Year

2025 Sedgwick data indicate that the number of vehicles affected fell to its lowest point in more than a decade.

Read More →

ASE Winter Registration Now Open

The deadline to register for the industry standard certification testing is March 31.

Read More →

U.S. Drivers Overdue for Major Services

Data shows dealers have ample opportunity ahead of the holiday travel season.

Read More →

Auto Dealers Losing Service Customers

Study finds that though overall service drive revenue is up, loyalty is eroding

Read More →

Jeeps Can Catch Fire

Hundreds of thousands recalled, some for second time, to address battery flaw

Read More →